Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS

Filed Pursuant to Rule 424(b)(2)

Registration No. 333-194465

The information in this preliminary prospectus supplement is not complete and may be changed. This preliminary prospectus supplement and the accompanying base prospectus are not an offer to sell these securities and are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH 12, 2014

P R E L I M I N A R Y P R O S P E C T U S S U P P L E M E N T

(To Prospectus dated March 10, 2014)

$

EnLink Midstream Partners, LP

$ % Senior Notes due 20

$ % Senior Notes due 20

$ % Senior Notes due 20

We are offering $ aggregate principal amount of our % Senior Notes due 20 , or the 20 notes, $ aggregate principal amount of our % Senior Notes due 20 , or the 20 notes, and $ aggregate principal amount of our % Senior Notes due 20 , or the 20 notes. We refer to the 20 notes, the 20 notes and the 20 notes, collectively, as the notes.

Interest on the notes will accrue from March , 2014 and will be payable semi-annually on and of each year, beginning on , 2014. The 20 notes will mature on , 20 , the 20 notes will mature on , 20 and the 20 notes will mature on , 20 . We may redeem some or all of the notes of each series at our option at any time and from time to time prior to their maturity at the applicable redemption prices set forth in this prospectus supplement, plus accrued and unpaid interest. Please read the section entitled "Description of Notes—Optional Redemption."

The notes will be our unsecured senior obligations. If we default, your right to payment under the notes will rank equally with the right to payment of the holders of our other current and future unsecured senior debt, including our existing senior notes and borrowings under our revolving credit facility, and senior in right of payment to all of our current and future subordinated debt. The notes will not initially be guaranteed by our subsidiaries.

Investing in the notes involves risks. See "Risk Factors" beginning on page S-11.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying base prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| |

Per 20 Note |

Total 20 Notes |

Per 20 Note |

Total 20 Notes |

Per 20 Note |

Total 20 Notes |

||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Public Offering Price |

% | $ | % | $ | % | $ | ||||||

Underwriting Discounts |

% | $ | % | $ | % | $ | ||||||

Proceeds to EnLink Midstream Partners, LP (before expenses) |

% | $ | % | $ | % | $ |

Interest on the notes will accrue from March , 2014 to the date of delivery.

The underwriters expect to deliver the notes to purchasers on or about March , 2014 only in book-entry form through the facilities of The Depository Trust Company for the accounts of its participants, including Euroclear Bank S.A./N.V., as operator of the Euroclear System, and Clearstream Banking, S.A.

Joint Book-Running Managers

| BofA Merrill Lynch | Citigroup | RBC Capital Markets | ||||

BMO Capital Markets |

Mitsubishi UFJ Securities |

BBVA |

Comerica Securities |

|||

J.P. Morgan |

RBS |

US Bancorp |

Wells Fargo Securities |

|||

March , 2014

We expect that delivery of the notes will be made to investors on or about March , 2014, which will be the business day following the date of this prospectus supplement (such settlement being referred to as "T+ "). Under Rule 15c6-1 under the Securities Exchange Act of 1934, as amended (the "Exchange Act"), trades in the secondary market are required to settle in three business days, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade notes on the date of this prospectus supplement or the next business days will be required, by virtue of the fact that the notes initially settle in T+ , to specify an alternate settlement arrangement at the time of any such trade to prevent a failed settlement. Purchasers of the notes who wish to trade the notes prior to their date of delivery hereunder should consult their advisors.

S-i

IMPORTANT INFORMATION IN THIS PROSPECTUS SUPPLEMENT

AND THE ACCOMPANYING BASE PROSPECTUS

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering of notes. The second part is the accompanying base prospectus, which describes certain terms of the indenture under which the notes will be issued and gives more general information, some of which may not apply to this offering of notes. Generally, when we refer only to the "prospectus," we are referring to both parts combined. If the information varies between this prospectus supplement and the accompanying base prospectus, you should rely on the information in this prospectus supplement.

Any statement made in this prospectus or in a document incorporated or deemed to be incorporated by reference into this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in this prospectus or in any other subsequently filed document that is also incorporated by reference into this prospectus modifies or supersedes that statement. Any statement so modified or superseded will not be deemed, except as so modified or superseded, to constitute a part of this prospectus. Please read "Information Incorporated by Reference" in this prospectus supplement.

You should rely only on the information contained in or incorporated by reference into this prospectus supplement, the accompanying base prospectus and any free writing prospectus prepared by or on behalf of us relating to this offering of notes. Neither we nor the underwriters have authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We and the underwriters are offering to sell the notes, and seeking offers to buy the notes, only in jurisdictions where offers and sales are permitted. You should not assume that the information contained in this prospectus supplement, the accompanying base prospectus or any free writing prospectus is accurate as of any date other than the dates shown in these documents or that any information we have incorporated by reference herein is accurate as of any date other than the date of the document incorporated by reference. Our business, financial condition, results of operations and prospects may have changed since such dates.

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

Some of the information included in this prospectus supplement and the documents we incorporate by reference herein contain "forward-looking" statements. All statements that are not statements of historical facts, including statements regarding our future financial position, business strategy, budgets, projected costs and plans and objectives of management for future operations, are forward-looking statements. You can typically identify forward-looking statements by the use of forward-looking words, such as "forecast," "may," "believe," "will," "should," "plan," "predict," "anticipate," "intend," "estimate," "expect" and other similar words. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this prospectus supplement, the accompanying base prospectus and the documents we have incorporated by reference.

These forward-looking statements are made based upon management's current plans, expectations, estimates, assumptions and beliefs concerning future events impacting us and therefore involve a number of risks and uncertainties. We caution that forward-looking statements are not guarantees and that actual results could differ materially from those expressed or implied in the forward-looking statements. Known material risks and uncertainties include the risks set forth under the heading "Risk Factors" in our Annual Report on Form 10-K for the year ended December 31, 2013 and our Current Report on Form 8-K dated March 7, 2014, as well as the following risks and uncertainties:

S-ii

Before you invest, you should be aware that the occurrence of any of the events described under the heading "Risk Factors" in our Annual Report on Form 10-K for the year ended December 31, 2013 and our Current Report on Form 8-K dated March 7, 2014 could substantially harm our business, results of operations and financial condition. In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

As generally used in the energy industry and in this prospectus supplement, the following terms have the following meanings:

S-iii

This summary highlights information contained elsewhere in this prospectus supplement and the accompanying base prospectus. It does not contain all of the information that you should consider before making an investment decision. You should read this entire prospectus supplement, the accompanying base prospectus and the documents incorporated herein by reference for a more complete understanding of this offering of notes. Please read "Risk Factors" beginning on page S-11 of this prospectus supplement and on page 1 of the accompanying base prospectus for information regarding risks you should consider before investing in our notes.

Throughout this prospectus supplement, when we use the terms "we," "us," "our" or the "Partnership," we are referring either to EnLink Midstream Partners, LP (formerly known as Crosstex Energy, L.P.) in its individual capacity or to EnLink Midstream Partners, LP and its operating subsidiaries collectively, as the context requires. Our business activities are conducted through our subsidiary, EnLink Midstream Operating, LP (formerly known as Crosstex Energy Services, L.P.), a Delaware limited partnership (the "Operating Partnership"), and the subsidiaries of the Operating Partnership. EnLink Midstream GP, LLC (formerly known as Crosstex Energy GP, LLC), a Delaware limited liability company, is our general partner. Our general partner is an indirect wholly owned subsidiary of EnLink Midstream, LLC ("ENLC"). ENLC's manager is an indirect wholly owned subsidiary of Devon Energy Corporation ("Devon").

Effective as of March 7, 2014, our Operating Partnership acquired 50% of the outstanding equity interests in EnLink Midstream Holdings, LP ("Midstream Holdings") and all of the outstanding equity interests in EnLink Midstream Holdings GP, LLC, the general partner of Midstream Holdings, from Devon. At the same time, Crosstex Energy, Inc. (to be renamed EnLink Midstream, Inc.) ("CEI"), the entity that directly owns our general partner, became a wholly owned subsidiary of ENLC. Another wholly owned subsidiary of ENLC owns the remaining 50% of the outstanding equity interests in Midstream Holdings.

Overview

EnLink Midstream Partners, LP is a publicly traded Delaware limited partnership formed in 2002. Our common units are traded on the New York Stock Exchange under the symbol "ENLK." We primarily focus on providing midstream energy services, including gathering, transmission, processing, fractionation and marketing, to producers of natural gas, NGLs, crude oil and condensate. We also provide crude oil, condensate and brine services to producers. Our midstream energy asset network includes approximately 7,300 miles of pipelines, 12 natural gas processing plants, six fractionators, 3.1 million barrels of NGL cavern storage, rail terminals, barge terminals, truck terminals and a fleet of approximately 100 trucks.

We connect the wells of natural gas producers in our market areas to our gathering systems, process natural gas for the removal of NGLs, fractionate NGLs into purity products and market those products for a fee, transport natural gas and ultimately provide natural gas to a variety of markets. We purchase natural gas from natural gas producers and other supply sources and sell that natural gas to utilities, industrial consumers, other marketers and pipelines. We operate processing plants that process gas transported to the plants by major interstate pipelines or from our own gathering systems under a variety of fee arrangements. We provide a variety of crude oil and condensate services throughout the Ohio River Valley, which include crude oil and condensate gathering via pipelines, barges, rail and trucks and brine disposal. We also have crude oil and condensate terminal facilities in south Louisiana that provide access for crude oil and condensate producers to the premium markets in this area. Our gas gathering systems consist of networks of pipelines that collect natural gas from points near producing wells and transport it to larger pipelines for further transmission. Our transmission pipelines primarily receive natural gas from our gathering systems and from third party gathering and transmission systems and deliver natural gas to industrial end-users, utilities and other pipelines. We also have transmission lines that transport NGLs from east Texas and our south Louisiana processing

S-1

plants to our fractionators in south Louisiana. Additionally, we own an economic interest in an NGL fractionator located at Mont Belvieu, Texas that receives raw mix NGLs from customers, fractionates the raw mix and redelivers the finished products to the customers for a fee. Devon is one of the largest customers of this fractionator. Our crude oil and condensate gathering and transmission systems consist of trucking facilities, pipelines, rail and barge facilities that, in exchange for a fee, transport oil from a producer site to an end user. Our processing plants remove NGLs and CO2 from a natural gas stream and our fractionators separate the NGLs into separate NGL products, including ethane, propane, iso-butane, normal butane and natural gasoline.

Our assets are comprised of systems and other assets in which our interest is held through our wholly-owned subsidiaries as well as systems and other assets owned by Midstream Holdings, in which we hold a 50% interest, and are located in four primary regions:

S-2

S-3

Our Business Strategies

Our primary business objectives are to have sustained growth in partnership distributions and to maintain a strong balance sheet. We intend to accomplish these objectives by executing the following strategies:

S-4

develop its oil and gas production. However, we cannot be certain that these opportunities will be made available to us, or that we will choose to pursue any such opportunity.

Our Competitive Strengths

We believe that we are well-positioned to execute our business strategies and to achieve our business objectives due to the following competitive strengths:

S-5

substantially all services that producers, marketers and others require to move natural gas, NGLs, crude oil and condensate from the wellhead to the market on a cost-effective basis.

Recent Developments

Tender Offer. Concurrently with this offering, we and our wholly owned subsidiary, EnLink Midstream Finance Corporation, announced a fixed price tender offer for any and all of the $725 million outstanding principal amount of our 8.875% Senior Notes due 2018 (the "2018 Notes") and a related solicitation of consents to certain proposed amendments to the indenture governing the 2018 Notes. We have offered to purchase the 2018 Notes for cash equal to $1,050 per $1,000 principal amount of the 2018 Notes tendered before 11:59 p.m., New York City time, on March 18, 2014, unless extended or earlier terminated by us, together with accrued and unpaid interest up to, but not including, the purchase date. This consideration includes a consent fee of $30 per $1,000 principal amount of 2018 Notes tendered.

Our tender offer and consent solicitation is being made on the terms and subject to the conditions set forth in an Offer to Purchase and Consent Solicitation Statement dated March 12, 2014. The tender offer and consent solicitation are conditioned upon our having obtained financing with terms and conditions satisfactory to us and in amounts not less than the amount required to purchase the 2018 Notes tendered in the tender offer. In addition, the tender offer and consent solicitation are conditioned upon the receipt of consents from holders of a majority of the outstanding principal amount of the 2018 Notes to eliminate substantially all of the restrictive covenants and certain events of default in the indenture governing the 2018 Notes.

If fully subscribed, we expect that the tender offer and consent solicitation will cost approximately $761.6 million (including the consent fee and expenses but excluding accrued and unpaid interest of approximately $6.1 million), which would be funded with the net proceeds from this offering, as described in "Use of Proceeds." There is no assurance that the tender offer, which is expected to be completed on March 19, 2014, will be subscribed for in any amount. In the event that all of the 2018 Notes are not tendered in the tender offer, or our tender offer and consent solicitation is not consummated, we will use a portion of the net proceeds from this offering to redeem any 2018 Notes that remain outstanding. The completion of this notes offering is not conditioned upon the completion of the tender offer and consent solicitation.

In connection with the tender offer and consent solicitation, we have retained Citigroup Capital Markets Inc. as the dealer manager. For a discussion of the terms of the 2018 Notes, see "Description of Other Indebtedness."

Devon Business Combination. Effective as of March 7, 2014, our Operating Partnership acquired (the "Acquisition") 50% of the outstanding equity interests in Midstream Holdings and all of the outstanding equity interests in EnLink Midstream Holdings GP, LLC, the general partner of Midstream Holdings, in exchange for the issuance by us of 120,542,441 units representing a new class of limited partnership interests in the Partnership. At the same time, CEI (to be renamed EnLink

S-6

Midstream, Inc.), the entity that directly owns our general partner, became a wholly owned subsidiary of ENLC (together with the Acquisition, the "business combination"). Another wholly owned subsidiary of ENLC owns the remaining 50% of the outstanding equity interests in Midstream Holdings.

Midstream Holdings was formerly a wholly-owned subsidiary of Devon and it gathers, processes and transports natural gas, primarily for Devon. Midstream Holdings also fractionates NGLs into component NGL products. Under the acquisition method of accounting, Midstream Holdings is considered the historical predecessor of our business because Devon obtained control of us through its control of ENLC and through the indirect acquisition our general partner.

Revolving Credit Facility. On February 20, 2014, we entered into a $1.0 billion unsecured revolving credit facility, which includes a $500.0 million letter of credit subfacility. Please see "Description of Other Indebtedness" for a description of our revolving credit facility.

Principal Executive Offices and Internet Address

Our principal executive offices are located at 2501 Cedar Springs Rd., Dallas, Texas 75201 and our telephone number is (214) 953-9500. Our website is located at www.enlink.com. We make available our periodic reports and other information filed with or furnished to the Securities and Exchange Commission, the "SEC" or the "Commission," free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the Commission. The information on our website is not part of this prospectus supplement or the accompanying base prospectus, and you should rely only on information contained or incorporated by reference in this prospectus supplement or the accompanying base prospectus when making a decision as to whether or not to invest in our notes.

S-7

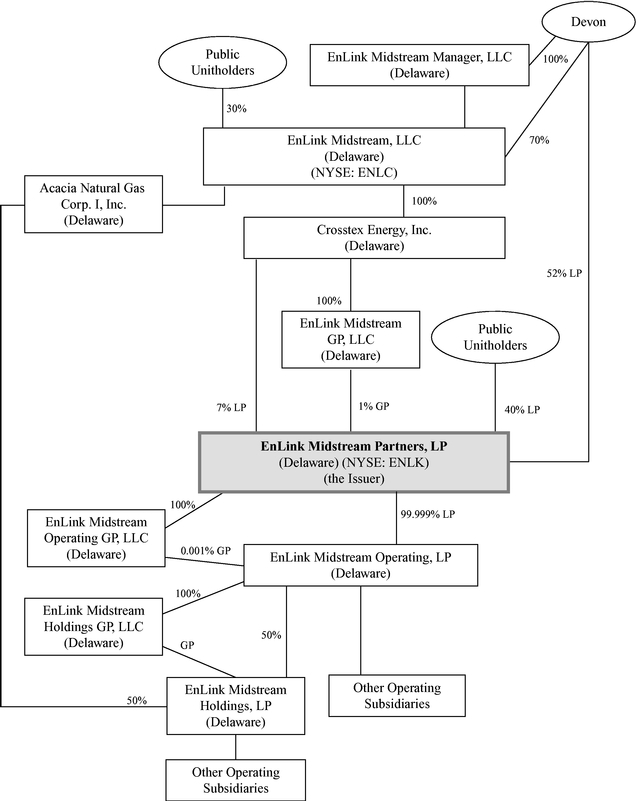

The diagram below depicts our organization and approximate ownership as of March 7, 2014.

Simplified Organizational Structure

S-8

We provide the following summary solely for your convenience. This summary is not a complete description of the notes. You should read the full text of, and more specific details contained elsewhere in, this prospectus supplement and the accompanying base prospectus. For a more detailed description of the notes, please read the section entitled "Description of Notes" in this prospectus supplement and the section entitled "Description of the Debt Securities" in the accompanying base prospectus.

| Issuer | EnLink Midstream Partners, LP | |

Notes Offered |

We are offering $ aggregate principal amount of notes consisting of the following series: |

|

|

• $ % Senior Notes due 20 ; |

|

|

• $ % Senior Notes due 20 ; and |

|

|

• $ % Senior Notes due 20 . |

|

Maturity |

Unless redeemed prior to maturity as described below, the 20 notes will mature on , 20 , the 20 notes will mature on , 20 and the 20 notes will mature on , 20 . |

|

Interest Rate |

Interest on the 20 notes will accrue at the per annum rate of %, interest on the 20 notes will accrue at the per annum rate of %, and interest on the 20 notes will accrue at the per annum rate of %. |

|

Interest Payment Dates |

Interest on the notes will accrue from, and including, the issue date of the notes and be payable semi-annually on and of each year, beginning on , 2014. |

|

Ranking |

The notes will be our unsecured senior obligations. The notes will rank equally with all of our other current and future unsecured senior debt, including our existing senior notes and borrowings under our revolving credit facility, senior to all of our current and future subordinated debt, and junior to the indebtedness and other obligations, including trade payables, of our subsidiaries. |

|

As of December 31, 2013, after giving effect to this offering of the notes and the application of the net proceeds therefrom as described in "Use of Proceeds" and the other transactions described under "Capitalization," we, excluding our subsidiaries, would have had $ billion of indebtedness outstanding, all of which would have been unsecured senior indebtedness, and our subsidiaries would have had approximately $22.0 million of indebtedness outstanding, consisting of capital leases. Please read "Description of Notes—Ranking." |

||

Optional Redemption |

We may redeem the notes of each series for cash, in whole or in part at any time and from time to time, at our option at the applicable redemption prices set forth under the heading "Description of Notes—Optional Redemption." |

S-9

| Certain Covenants | We will issue the notes under a supplement to an indenture with Wells Fargo Bank, National Association, as trustee. The covenants in the indenture supplement will include a limitation on liens and a restriction on sale-leaseback transactions. Each covenant is subject to a number of important exceptions, limitations and qualifications that are described in "Description of Notes—Certain Covenants." | |

Use of Proceeds |

We intend to use the net proceeds from this offering to fund our pending tender offer and consent solicitation for the 2018 Notes, to reduce borrowings under our revolving credit facility and for general partnership purposes, including growth capital expenditures. In the event that all of the 2018 Notes are not tendered in the tender offer or our tender offer is not consummated, we will use a portion of the net proceeds from this offering to redeem any 2018 Notes that remain outstanding. See "Use of Proceeds." |

|

Affiliates of each of the underwriters are lenders under our revolving credit facility that we expect to reduce using a portion of the proceeds of this offering, and affiliates of certain of the underwriters are holders of our 2018 Notes that we intend to repurchase or redeem using a portion of the proceeds of this offering and, accordingly, such underwriters and affiliates will receive a portion of the proceeds from this offering. See "Underwriting." |

||

Further Issuances |

We may create and issue additional notes ranking equally and ratably with any series of notes offered by this prospectus supplement in all respects, except for the issue date, issue price and in some cases, the first interest payment date, so that such additional notes will form a single series with the applicable series of notes offered by this prospectus supplement and will have substantially identical terms as such series, including with respect to ranking, redemption and otherwise. |

|

Risk Factors |

Investing in the notes involves risks. See "Risk Factors" beginning on page S-11 of this prospectus supplement and the risk factors set forth on page 1 of the accompanying base prospectus, and in our Annual Report on Form 10-K for the year ended December 31, 2013 and in our Current Report on Form 8-K dated March 7, 2014, together with all of the other information included in, or incorporated by reference into, this prospectus supplement and the accompanying base prospectus before investing in the notes. |

|

Governing Law |

The indenture governing the notes and the notes will be governed by, and construed in accordance with, the laws of the State of New York. |

S-10

An investment in the notes involves risks. You should consider carefully the following risk factors and the risk factors set forth beginning on page 1 of the accompanying base prospectus and in our Annual Report on Form 10-K for the year ended December 31, 2013 and in our Current Report on Form 8-K dated March 7, 2014, together with all of the other information included in, or incorporated by reference into, this prospectus supplement and the accompanying base prospectus when evaluating an investment in the notes.

Risks Related to the Notes

Our significant indebtedness, and any future indebtedness, as well as the restrictions in our debt agreements may adversely affect our future financial and operating flexibility and our ability to service the notes.

As of December 31, 2013, after giving effect to this offering and the application of the net proceeds as described in "Use of Proceeds" and the other transactions described under "Capitalization," our consolidated indebtedness would have been $ million, and we would have been able to incur an additional $ million of indebtedness under our revolving credit facility. Our substantial indebtedness and the additional debt we may incur in the future for potential acquisitions or operating activities may adversely affect our liquidity and therefore our ability to make interest payments on the notes.

Among other things, our significant indebtedness may be viewed negatively by credit rating agencies, which could result in increased costs for us to access the capital markets. Any future downgrade of the debt issued by us or our subsidiaries could significantly increase our capital costs or adversely affect our ability to raise capital in the future.

Debt service obligations and restrictive covenants in our revolving credit facility and other indebtedness and the indenture governing the notes may adversely affect our ability to finance future operations, pursue acquisitions and fund other capital needs. In addition, this leverage may make our results of operations more susceptible to adverse economic or operating conditions by limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate and may place us at a competitive disadvantage as compared to our competitors that have less debt.

The indenture governing the notes will permit us to incur additional debt, which would be equal in right of payment to the notes. If we incur any additional indebtedness, including trade payables, that ranks equally with the notes, the holders of that debt would be entitled to share ratably with you in any proceeds distributed in connection with any insolvency, liquidation, reorganization, dissolution or other winding up of us. This may have the effect of reducing the amount of proceeds paid to you. If new debt is added to our current debt levels, the related risks that we now face could intensify.

The notes will be our senior unsecured obligations and as a result, the notes will be effectively junior to our future secured indebtedness, to the extent of the value of the collateral securing such indebtedness, and structurally subordinated to the indebtedness and other liabilities of our subsidiaries, other than subsidiaries that may guarantee the notes in the future.

The notes will be our senior unsecured obligations and will rank equally in right of payment with all of our other existing and future senior indebtedness, and will be structurally subordinated to the claims of all creditors, including trade creditors and tort claimants, of our subsidiaries, other than subsidiaries that may guarantee the notes in the future. In the event of the liquidation, dissolution, reorganization, bankruptcy or similar proceeding of the business of a subsidiary that is not a guarantor, creditors of that subsidiary, including trade creditors, would generally have the right to be paid in full before any distribution is made to us or the holders of the notes. Accordingly, there may not be sufficient funds remaining to pay amounts due on all or any of the notes. As of December 31, 2013, after giving effect to the transactions described under "Capitalization," our subsidiaries would have had

S-11

approximately $22.0 million of indebtedness outstanding, consisting of capital leases. The indenture will not prohibit such subsidiaries from incurring indebtedness in the future.

In addition, because the notes are, and any future guarantees of the notes will be, unsecured, holders of any secured indebtedness of ours or our subsidiaries would have claims with respect to the assets constituting collateral for such indebtedness that are senior to the claims of the holders of the notes. Currently, neither we nor any of our subsidiaries has any secured indebtedness. Although the indenture governing the notes will place some limitations on our ability to create liens securing indebtedness, there will be significant exceptions to these limitations that would allow us to secure significant amounts of indebtedness without equally and ratably securing the notes. If we or our subsidiaries incur secured indebtedness and such indebtedness is accelerated or we become subject to bankruptcy, liquidation or reorganization proceedings, our and our subsidiaries' assets would be used to satisfy obligations with respect to the indebtedness secured thereby before any payment could be made on the notes. Consequently, any such secured indebtedness would effectively be senior to the notes and any future guarantees of the notes, to the extent of the value of the collateral securing such secured indebtedness. In that event, you may not be able to recover all the principal or interest you are due under the notes.

Any future subsidiary guarantees could be deemed fraudulent conveyances under certain circumstances, and in such event a court may try to subordinate or void the subsidiary guarantees.

Initially, none of our subsidiaries will guarantee the notes, although in the future one or more of our subsidiaries may do so. Under the federal bankruptcy laws and comparable provisions of state fraudulent transfer laws, a subsidiary guarantee could be voided, or claims in respect of a subsidiary guarantee could be subordinated to all other debts of that subsidiary guarantor if, among other things, the subsidiary guarantor, at the time it incurred the indebtedness evidenced by its subsidiary guarantee received less than reasonably equivalent value or fair consideration for the incurrence of such subsidiary guarantee; and

In addition, any payment by that subsidiary guarantor pursuant to its subsidiary guarantee could be voided and required to be returned to the subsidiary guarantor, or to a fund for the benefit of the creditors of the subsidiary guarantor. The measures of insolvency for purposes of these fraudulent transfer laws will vary depending upon the law applied in any proceeding to determine whether a fraudulent transfer has occurred. Generally, however, a subsidiary guarantor would be considered insolvent if:

S-12

We will make only limited covenants in the indenture governing the notes and these limited covenants may not protect your investment.

The indenture governing the notes will not:

The indenture will also permit us and our subsidiaries to incur additional indebtedness, including secured indebtedness, that could effectively rank senior to the notes, and to engage in leaseback arrangements, subject to certain limitations. Any of these actions could adversely affect our ability to make principal and interest payments on the notes.

We have a holding company structure in which our subsidiaries conduct our operations and own our operating assets.

We are a holding company, and our subsidiaries conduct all of our operations and own all of our operating assets. We do not have significant assets other than the equity in our subsidiaries. As a result, our ability to make required payments on the notes depends on the performance of our subsidiaries and their ability to distribute funds to us. The ability of our subsidiaries to make distributions to us may be restricted by, among other things, credit instruments and applicable state partnership laws and other laws and regulations. If our subsidiaries are prevented from distributing funds to us, we may be unable to pay all the principal and interest on the notes when due.

We do not have the same flexibility as other types of organizations to accumulate cash, which may limit cash available to service the notes or to repay them at maturity.

Unlike a corporation, we are required by our partnership agreement to distribute, on a quarterly basis, 100% of our available cash to our unitholders of record and our general partner. "Available cash" is defined in our partnership agreement, and it generally means, for each fiscal quarter:

S-13

As a result, we do not expect to accumulate significant amounts of cash. Depending on the timing and amount of our cash distributions, these distributions could significantly reduce the cash available to us in subsequent periods to make payments on the notes.

Your ability to transfer the notes at a time or price you desire may be limited by the absence of an active trading market, which may not develop.

The notes are new issues of securities for which there are no established public markets. Although we have registered the offer and sale of the notes under the Securities Act of 1933, as amended ("the Securities Act"), we do not intend to apply for the listing of the notes on any securities exchange or for the quotation of the notes on any automated dealer quotation system. In addition, although the underwriters have informed us that they intend to make a market in the notes of each series, as permitted by applicable laws and regulations, they are not obligated to make markets in the notes, and they may discontinue their market-making activities at any time without notice. Active markets for the notes may not develop or, if developed, may not continue. In the absence of active trading markets, you may not be able to transfer the notes within the time or at the prices you desire.

We may not be able to generate sufficient cash to service all of our indebtedness, including the notes, our existing notes and our indebtedness under our revolving credit facility, and we may be forced to take other actions to satisfy our obligations under our indebtedness, which may not be successful.

Our ability to make scheduled payments on or to refinance our debt obligations depends on our financial and operating performance, which is subject to prevailing economic and competitive conditions and to certain financial, business and other factors beyond our control. We cannot assure you that we will maintain a level of cash flows from operating activities sufficient to permit us to pay the principal, premium, if any, and interest on our indebtedness.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets or operations, seek additional capital or restructure or refinance our indebtedness, including the notes. We cannot assure you that we would be able to take any of these actions, that these actions would be successful and would permit us to meet our scheduled debt service obligations or that these actions would be permitted under the terms of our existing or future debt agreements, including our credit agreement, the indentures governing our existing notes and the indenture that will govern the notes. For example, our revolving credit facility contains restrictions on our ability to dispose of assets. We may not be able to consummate asset dispositions, and any proceeds may not be adequate to meet any debt service obligations then due. See "Description of Other Indebtedness" and "Description of Notes."

The credit and risk profile of our general partner and its owner could adversely affect our credit ratings and profile.

The credit and business risk profiles of our general partner and its indirect owner, Devon, may be factors in credit evaluations of us due to the control of our general partner, the significant business we conduct with Devon and the significant influence over our business activities, including our cash distributions, acquisition strategy and business risk profile. Another factor that may be considered is the financial condition of our general partner and Devon, including the degree of their financial leverage.

S-14

Our tax treatment will depend on our status as a partnership for U.S. federal income tax purposes, as well as our not being subject to entity-level taxation by individual states. If the Internal Revenue Service (the "IRS") treats us as a corporation for tax purposes or we become subject to additional entity-level taxation, it would reduce the amount of cash available for payment of principal and interest on the notes.

If we were classified as a corporation for U.S. federal income tax purposes, we would be required to pay U.S. federal income tax on our taxable income at the corporate tax rate, which is currently a maximum of 35%, and would likely pay state income tax at varying rates. Treatment of us as a corporation would cause a material reduction in our anticipated cash flow, which could materially and adversely affect our ability to make payments on the notes.

Current law may change so as to cause us to be treated as a corporation for U.S. federal income tax purposes or otherwise subject us to entity-level taxation. For example, at the federal level, legislation previously has been proposed that would eliminate partnership tax treatment for certain publicly traded partnerships. Although such proposed legislation would not have applied to us as proposed, it is possible that modified versions of such legislation could be enacted which would apply to us. We are unable to predict whether any of these changes, or other proposals, will ultimately be enacted. Any such changes could materially and adversely affect our ability to make payments on the notes. At the state level, because of widespread state budget deficits and for other reasons, several states are evaluating ways to subject partnerships to entity-level taxation through the imposition of state income, franchise and other forms of taxation. For example, as a partnership operating in Texas we are required to pay franchise tax at a maximum effective rate of 0.7% of our gross income apportioned to Texas. If any other state were to impose a tax on us, the cash we have available to make payments on the notes could be materially reduced.

S-15

We expect to receive net proceeds from this offering of approximately $ million after deducting the underwriting discounts and estimated offering expenses payable by us.

We will use approximately $767.7 million of the net proceeds from this offering to fund our pending tender offer and consent solicitation for the 2018 Notes, including the consent fee, expenses and accrued and unpaid interest. In the event that all of the 2018 Notes are not tendered in our tender offer, or our tender offer and consent solicitation is not consummated, we will use a portion of the net proceeds from this offering to redeem any 2018 Notes that remain outstanding. We will use the remaining net proceeds from this offering to reduce outstanding borrowings under our revolving credit facility and for general partnership purposes, including growth capital expenditures.

As of March 7, 2014, we had $725.0 million in aggregate principal amount of 2018 Notes outstanding. Interest on the 2018 Notes accrues at the rate of 8.875% per annum and the 2018 Notes will mature on February 15, 2018.

As of March 7, 2014, we had $397.0 million in borrowings and $58.7 million in outstanding letters of credit under our $1.0 billion revolving credit facility at a weighted average interest rate of 3.5%. Our revolving credit facility matures in March 2019, unless we request, and the requisite lenders agree, to extend it pursuant to its terms. Borrowings under our revolving credit facility were used to repay outstanding borrowings under our prior credit facility. Borrowings under our prior credit facility were used for general partnership purposes, including growth capital expenditures. Please read "Description of Other Indebtedness—Credit Agreement" for a description of our revolving credit facility.

Affiliates of each of the underwriters are lenders under our revolving credit facility that we expect to reduce using a portion of the proceeds from this offering, and affiliates of certain of the underwriters are holders of our 2018 Notes that we intend to redeem using a portion of the proceeds of this offering and, accordingly, such underwriters and affiliates will receive a portion of the proceeds from this offering. See "Underwriting."

S-16

The following table sets forth our cash and cash equivalents and our capitalization as of December 31, 2013:

You should read this table in conjunction with our financial statements and notes that are incorporated by reference into this prospectus supplement and the accompanying base prospectus for additional information about our capital structure.

| |

As of December 31, 2013 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Historical | Pro forma | Pro forma As Adjusted |

|||||||

| |

(In millions) |

|||||||||

Cash and cash equivalents |

— | $ | 0.1 | $ | ||||||

| | | | | | | | | | | |

| | | | | | | | | | | |

Long-term debt including current maturities: |

||||||||||

Revolving credit facility(1) |

— | $ | 155.0 | |||||||

8.875% Senior Notes due 2018 (including premium of $37.2 million(2)) |

— | 762.2 | — | (3) | ||||||

7.125% Senior Notes due 2022 (including premium of $34.4 million(2)) |

— | 284.4 | 223.5 | (4) | ||||||

20 Notes offered hereby |

— | — | ||||||||

20 Notes offered hereby |

— | — | ||||||||

20 Notes offered hereby |

— | — | ||||||||

| | | | | | | | | | | |

Total long-term debt including current maturities |

— | 1,201.6 | ||||||||

Partners' equity: |

||||||||||

EnLink Midstream Partners, LP equity |

— | 4,478.3 | 4,478.3 | |||||||

Predecessor |

$ | 1,783.7 | — | — | ||||||

Non-controlling interest |

— | 1,107.5 | 1,107.5 | |||||||

| | | | | | | | | | | |

Total partners' equity |

1,783.7 | 5,585.8 | 5,585.8 | |||||||

| | | | | | | | | | | |

Total capitalization |

$ | 1,783.7 | $ | 6,787.4 | $ | |||||

| | | | | | | | | | | |

| | | | | | | | | | | |

S-17

purchased may be less. In the event that all of the 2018 Notes are not tendered or our tender offer and consent solicitation is not consummated, we will use a portion of the net proceeds from this offering to redeem any 2018 Notes that remain outstanding.

S-18

DESCRIPTION OF OTHER INDEBTEDNESS

Credit Agreement

On February 20, 2014, we entered into a credit agreement (the "credit agreement"), with Bank of America, N.A., as Administrative Agent, Swing Line Lender and L/C Issuer, Citibank, N.A. and Wells Fargo Bank, National Association, as Co-Syndication Agents, Royal Bank of Canada and Bank of Montreal, as Co-Documentation Agents, and the other lenders party thereto. The credit agreement permits us to borrow up to $1.0 billion on a revolving credit basis and includes a $500.0 million letter of credit subfacility. Our obligations under the credit agreement are unsecured, and our subsidiaries are not required to guarantee our obligations thereunder.

The credit agreement matures in March 2019, unless we request, and the requisite lenders agree, to extend it pursuant to its terms. The credit agreement contains certain financial, operational and legal covenants. Among other things, these covenants include maintaining a ratio of consolidated indebtedness to consolidated EBITDA (as defined in the credit agreement, which definition includes projected EBITDA from certain capital expansion projects) of no more than 5.0 to 1.0. If we consummate one or more acquisitions in which the aggregate purchase price is $50.0 million or more, the maximum allowed ratio of consolidated indebtedness to consolidated EBITDA will increase to 5.5 to 1.0 for the quarter of the acquisition and the three following quarters. Upon breach by us of certain covenants, amounts outstanding under the credit agreement, if any, may become due and payable immediately.

Borrowings under the credit agreement bear interest at our option at the Eurodollar Rate (the LIBOR Rate) plus an applicable margin or the Base Rate (the highest of the Federal Funds Rate plus 0.50%, the 30-day Eurodollar Rate plus 1.0%, or the administrative agent's prime rate) plus an applicable margin. The applicable margins vary depending on our credit rating. As of March 7, 2014, we had $397.0 million in borrowings and $58.7 million in outstanding letters of credit under our revolving credit facility.

Senior Notes Due 2018

On February 10, 2010, we issued $725.0 million in aggregate principal amount of the 2018 Notes. Interest on the 2018 Notes accrues at the rate of 8.875% per annum and is payable semi-annually in arrears on each February 15 and August 15. The 2018 Notes will mature on February 15, 2018.

On or after February 15, 2014, we may redeem all or a part of the 2018 Notes at redemption prices (expressed as percentages of principal amount) equal to 104.438% for the twelve-month period beginning on February 15, 2014, 102.219% for the twelve-month period beginning February 15, 2015 and 100.00% for the twelve-month period beginning on February 15, 2016 and at any time thereafter, in each case plus accrued and unpaid interest, if any, to the applicable redemption date on the 2018 Notes.

The indenture governing the 2018 Notes contains covenants that, among other things, limit our ability and the ability of certain of our subsidiaries to: (i) sell assets, including equity interests in our subsidiaries; (ii) pay distributions on, redeem or repurchase units or redeem or repurchase our subordinated debt; (iii) make investments; (iv) incur or guarantee additional indebtedness or issue preferred units; (v) create or incur certain liens; (vi) enter into agreements that restrict distributions or other payments from our restricted subsidiaries to us; (vii) consolidate, merge or transfer all or substantially all of our assets; (viii) engage in transactions with affiliates; (ix) create unrestricted subsidiaries; (x) enter into sale and leaseback transactions; or (xi) engage in certain business activities. These covenants are subject to a number of important exceptions and qualifications. As of December 31, 2013, we were in compliance with all of the covenants included in the indenture governing the 2018 Notes.

S-19

We intend to use the net proceeds from this offering to repurchase or redeem all of the 2018 Notes.

Senior Notes Due 2022

On May 24, 2012, we issued $250.0 million in aggregate principal amount of the 2022 Notes. Interest on the 2022 Notes accrues at the rate of 7.125% per annum and is payable semi-annually in arrears on each June 1 and December 1. The 2022 Notes will mature on June 1, 2022.

We may redeem up to 35% of the 2022 Notes at any time prior to June 1, 2015 in an amount not greater than the cash proceeds from equity offerings at a redemption price of 107.125% of the principal amount of the 2022 Notes (plus accrued and unpaid interest to the redemption date). Pursuant to the foregoing, on February 2, 2014, we redeemed approximately $53.5 million in aggregate principal amount of the 2022 Notes (the "Redeemed Notes"), representing approximately 21% of the aggregate principal amount of the outstanding 2022 Notes, for a total redemption price equal to $1,083.32 per $1,000 principal amount redeemed. Following the completion of the redemption, approximately $196.5 million aggregate principal amount of the 2022 Notes remain outstanding.

Prior to June 1, 2017, we may redeem the 2022 Notes, in whole or in part, at a "make-whole" redemption price. On or after June 1, 2017, we may redeem all or a part of the 2022 Notes at redemption prices (expressed as percentages of principal amount) equal to 103.563% for the twelve-month period beginning on June 1, 2017, 102.375% for the twelve-month period beginning on June 1, 2018, 101.188% for the twelve-month period beginning on June 1, 2019 and 100.00% for the twelve-month period beginning on June 1, 2020 and at any time thereafter, in each case plus accrued and unpaid interest, if any, to the applicable redemption date on the 2022 Notes.

The indenture governing the 2022 Notes contains covenants that, among other things, limit our ability and the ability of certain of our subsidiaries to: (i) sell assets, including equity interests in our subsidiaries; (ii) pay distributions on, redeem or repurchase units or redeem or repurchase our subordinated debt; (iii) make investments; (iv) incur or guarantee additional indebtedness or issue preferred units; (v) create or incur certain liens; (vi) enter into agreements that restrict distributions or other payments from our restricted subsidiaries to us; (vii) consolidate, merge or transfer all or substantially all of our assets; (viii) engage in transactions with affiliates; (ix) create unrestricted subsidiaries; (x) enter into sale and leaseback transactions; or (xi) engage in certain business activities. These covenants are subject to a number of important exceptions and qualifications. As of December 31, 2013, we were in compliance with all of the covenants included in the indenture governing the 2022 Notes.

If the 2022 Notes achieve an investment grade rating from each of Moody's Investors Service, Inc. and Standard & Poor's Ratings Services, many of these covenants will terminate.

S-20

At the closing of this offering, we will enter into a base indenture between us and Wells Fargo Bank, National Association, as trustee, pursuant to which we may issue multiple series of debt securities from time to time. We will issue the notes under such base indenture, as supplemented by a supplemental indenture setting forth the specific terms of the notes (as so supplemented, the "indenture"). This description is a summary of the material provisions of the notes and the indenture. This description does not restate those agreements and instruments in their entirety. You should refer to the notes and the indenture, forms of which are available as set forth below under "Available Information," for a complete description of our obligations and your rights.

The following description of the particular terms of the notes supplements the general description of the debt securities included in the accompanying base prospectus under the caption "Description of the Debt Securities." The notes offered hereby will be a series of senior debt securities issued by us as described herein and therein. You should review this "Description of Notes" together with the "Description of the Debt Securities" included in the accompanying base prospectus. To the extent that this "Description of Notes" is inconsistent with the "Description of the Debt Securities" in the accompanying base prospectus, this "Description of Notes" will control and replace the inconsistent "Description of the Debt Securities" in the accompanying base prospectus.

You can find the definitions of various terms used in this description under "—Certain Definitions" below. In this description, the terms "EnLink Midstream," "we," "us" and "our" refer only to EnLink Midstream Partners, LP and not to any of its Subsidiaries.

General

The notes:

The 20 notes, the 20 notes and the 20 notes each constitute a separate series of debt securities under the indenture. The indenture does not limit the amount of debt securities we may issue under the indenture from time to time in one or more series. We may in the future issue additional debt securities under the indenture in addition to the notes as described below under "—Further Issuances."

Interest

Interest on the notes will accrue from and including March , 2014 or from and including the most recent interest payment date to which interest has been paid or provided for. We will pay interest

S-21

in cash semi-annually in arrears on and of each year, beginning , 2014. We will make interest payments to the persons in whose names the notes are registered at the close of business on or , as applicable, before the next interest payment date. Interest will be computed on the basis of a 360-day year consisting of twelve 30-day months. If any interest payment date falls on a day that is not a business day, the payment will be made on the next business day, and no interest will accrue on the amount of interest due on that interest payment date for the period from and after the interest payment date to the date of payment.

Paying Agent and Registrar

The trustee will initially act as paying agent and registrar for the notes. We may change the paying agent or registrar without prior notice to the holders of the notes, and we or any of our Subsidiaries may act as paying agent or registrar; provided, however, that we will be required to maintain at all times an office or agency in The City of New York (which may be an office of the trustee or an affiliate of the trustee or the registrar or a co-registrar for the notes) where the notes may be presented for payment and where notes may be surrendered for registration of transfer or for exchange and where notices and demands to or upon us in respect of the notes and the indenture may be served. We may also from time to time designate one or more additional offices or agencies where the notes may be presented or surrendered for any or all such purposes and may from time to time rescind such designations.

Further Issuances

We may from time to time, without notice to or the consent of the holders of the notes, create and issue additional notes having the same terms as any of the series of notes offered by this prospectus supplement and accompanying base prospectus, except for issue date, issue price and in some cases, the first interest payment date. Additional notes issued in this manner will form a single series with the previously issued and outstanding notes of such series.

Optional Redemption

Prior to , 20 , with respect to the 20 notes ( months prior to their maturity date), 20 , with respect to the 20 notes ( months prior to their maturity date), and , 20 , with respect to the 20 notes ( months prior to their maturity date), the respective notes will be redeemable, at our option, at any time in whole, or from time to time in part, at a price equal to the greater of:

plus, in either case, accrued and unpaid interest to, but excluding, the redemption date.

At any time on or after , 20 , with respect to the 20 notes ( months prior to their maturity date), 20 , with respect to the 20 notes ( months prior to their maturity date), and , 20 , with respect to the 20 , notes ( months prior to their maturity date), the respective notes will be redeemable in whole or in part, at our option, at a redemption price equal to

S-22

100% of the principal amount of the notes to be redeemed plus accrued and unpaid interest thereon to, but excluding, the redemption date.

For purposes of determining the redemption price, the following definitions are applicable:

"Comparable Treasury Issue" means the United States Treasury security selected by the Quotation Agent as having a maturity comparable to the remaining term of the notes to be redeemed that would be utilized, at the time of selection and in accordance with customary financial practice, in pricing new issues of corporate debt securities of comparable maturity to the remaining term of such notes.

"Comparable Treasury Price" means, with respect to any redemption date for notes, (1) the average of four Reference Treasury Dealer Quotations for such redemption date after excluding the highest and lowest of all of the Reference Treasury Dealer Quotations or (2) if the Quotation Agent obtains fewer than four such Reference Treasury Dealer Quotations, the average of all such quotations.

"Quotation Agent" means the Reference Treasury Dealer appointed by us.

"Primary Treasury Dealer" means a U.S. government securities dealer in the United States.

"Reference Treasury Dealer" means (i) each of Citigroup Global Markets Inc. and Merrill Lynch, Pierce, Fenner & Smith Incorporated and their respective successors and (ii) two other Primary Treasury Dealers selected by us.

"Reference Treasury Dealer Quotation" means, with respect to each Reference Treasury Dealer and any redemption date, the average, as determined by the Quotation Agent, of the bid and asked prices for the Comparable Treasury Issue (expressed in each case as a percentage of its principal amount) quoted in writing to the Quotation Agent by such Reference Treasury Dealer at 5:00 p.m., New York City time, on the third business day preceding the redemption date.

"Treasury Rate" means, with respect to any redemption date, the rate per year equal to the semi-annual equivalent yield to maturity of the Comparable Treasury Issue, calculated using a price for the Comparable Treasury Issue (expressed as a percentage of its principal amount) equal to the Comparable Treasury Price for such redemption date. The Treasury Rate will be calculated on the third business day preceding any redemption date.

Redemption Procedures

If fewer than all of the notes of a series are to be redeemed at any time, such notes will be selected for redemption not more than 60 days prior to the redemption date and such selection will be made by the trustee on a pro rata basis, by lot or by such other method as the trustee deems appropriate (or, in the case of notes represented by a note in global form, by such method as The Depository Trust Company ("DTC") may require); provided, that no partial redemption of any note will occur if such redemption would reduce the principal amount of such note to less than $2,000. Notices of redemption with respect to the notes will be sent at least 30 but not more than 60 days before the redemption date to each holder of notes to be redeemed.

If any note is to be redeemed in part only, the notice of redemption that relates to such note will state the portion of the principal amount thereof to be redeemed. A new note in principal amount equal to the unredeemed portion thereof will be issued in the name of the holder thereof upon cancellation of the original note. Notes called for redemption will become due on the date fixed for redemption. Unless we default in payment of the redemption price, on and after the redemption date, interest will cease to accrue on the notes or portions of the notes called for redemption.

S-23

Future Subsidiary Guarantees

The notes initially will not be guaranteed by any of our Subsidiaries. However, if at any time following the issuance of the notes, any Subsidiary of EnLink Midstream becomes a guarantor or co-obligor of our Credit Agreement, then EnLink Midstream will cause such Subsidiary to promptly execute and deliver to the trustee a supplemental indenture in a form satisfactory to the trustee pursuant to which such Subsidiary guarantees EnLink Midstream's obligations with respect to the notes on the terms provided for in the indenture.

The guarantee of any Subsidiary Guarantor may be released under certain circumstances. If we exercise our legal or covenant defeasance option with respect to the notes as described below under "—Defeasance and Discharge," then any Subsidiary Guarantor will be released. Further, if no default has occurred and is continuing under the indenture, and to the extent not otherwise prohibited by the indenture, a Subsidiary Guarantor will be unconditionally released and discharged from its guarantee:

If at any time following any release of a Subsidiary Guarantor from its guarantee of the notes pursuant to the third bullet point in the preceding paragraph, the Subsidiary Guarantor again becomes a guarantor or co-obligor of our Credit Agreement, then EnLink Midstream will cause the Subsidiary Guarantor to again guarantee the notes in accordance with the indenture.

Ranking

The notes will be unsecured, unless we are required to secure them pursuant to the limitations on liens covenant described below under "—Certain Covenants—Limitations on Liens." The notes will also be the unsubordinated obligations of EnLink Midstream and will rank equally with all other existing and future unsubordinated indebtedness of EnLink Midstream. Each guarantee, if any, of the notes will be an unsecured and unsubordinated obligation of the Subsidiary Guarantor and will rank equally with all other existing and future unsubordinated indebtedness of the Subsidiary Guarantor. The notes and each guarantee, if any, will effectively rank junior to any future indebtedness of EnLink Midstream and any Subsidiary Guarantor that is both secured and unsubordinated to the extent of the value of the assets securing such indebtedness, and the notes will structurally rank junior to all indebtedness and other liabilities of EnLink Midstream's existing and future Subsidiaries that are not Subsidiary Guarantors.

As of December 31, 2013, after giving effect to this offering of the notes and the application of the net proceeds therefrom as described in "Use of Proceeds" and the other transactions described under "Capitalization," EnLink Midstream, excluding its Subsidiaries, would have had $ billion of indebtedness outstanding, all of which would have been unsecured, unsubordinated indebtedness, consisting entirely of the notes and our existing 2022 Notes. Initially, none of EnLink Midstream's Subsidiaries will guarantee the notes. As of December 31, 2013, after giving effect to this offering of the notes and the application of the net proceeds therefrom as described in "Use of Proceeds" and the other transactions described under "Capitalization," these Subsidiaries would have had approximately $22.0 million of indebtedness outstanding, consisting of capital leases.

S-24

Open Market Purchases; No Mandatory Redemption or Sinking Fund

We may at any time and from time to time repurchase notes in the open market or otherwise, in each case without any restriction under the indenture. We are not required to make any mandatory redemption or sinking fund payments with respect to the notes.

Certain Covenants

Except as set forth below, neither EnLink Midstream nor any of its Subsidiaries is restricted by the indenture from incurring any type of indebtedness or other obligation, from paying dividends or making distributions on its partnership or other equity interests or from purchasing or redeeming its partnership or other equity interests. The indenture does not require the maintenance of any financial ratios or specified levels of net worth or liquidity. In addition, the indenture does not contain any provisions that would require EnLink Midstream to repurchase or redeem or otherwise modify the terms of the notes upon a change in control or other events involving EnLink Midstream that could adversely affect the creditworthiness of EnLink Midstream.

Limitations on Liens. EnLink Midstream will not, nor will it permit any of its Principal Subsidiaries to, create, assume, incur or suffer to exist any mortgage, lien, security interest, pledge, charge or other encumbrance ("liens") upon any Principal Property or upon any capital stock of any Principal Subsidiary, whether owned on the date of the supplemental indenture creating the notes or thereafter acquired, to secure any Indebtedness of EnLink Midstream or any other Person (other than the notes), without in any such case making effective provisions whereby all of the outstanding notes are secured equally and ratably with, or prior to, such Indebtedness so long as such Indebtedness is so secured.

Notwithstanding the foregoing, under the indenture, EnLink Midstream may, and may permit any of its Principal Subsidiaries to, create, assume, incur, or suffer to exist without securing the notes (a) any Permitted Lien, (b) any lien upon any Principal Property or capital stock of a Principal Subsidiary to secure Indebtedness of EnLink Midstream or any other Person, provided that the aggregate principal amount of all Indebtedness then outstanding secured by such lien and all similar liens under this clause (b), together with all Attributable Indebtedness from Sale-Leaseback Transactions (excluding Sale-Leaseback Transactions permitted by clauses (1) through (4), inclusive, of the first paragraph of the restriction on sale-leasebacks covenant described below), does not exceed 15% of Consolidated Net Tangible Assets or (c) any lien upon (i) any Principal Property that was not owned by EnLink Midstream or any of its Subsidiaries on the date of the supplemental indenture creating the notes or (ii) the capital stock of any Principal Subsidiary that owns no Principal Property that was owned by EnLink Midstream or any of its Subsidiaries on the date of the supplemental indenture creating the notes, in each case owned by a Subsidiary of EnLink Midstream (an "Excluded Subsidiary") that (A) is not, and is not required to be, a Subsidiary Guarantor and (B) has not granted any liens on any of its property securing Indebtedness with recourse to EnLink Midstream or any Subsidiary of EnLink Midstream other than such Excluded Subsidiary or any other Excluded Subsidiary.

Restriction on Sale-Leasebacks. EnLink Midstream will not, and will not permit any Principal Subsidiary to, engage in the sale or transfer by EnLink Midstream or any of its Principal Subsidiaries of any Principal Property to a Person (other than EnLink Midstream or a Principal Subsidiary) and the taking back by EnLink Midstream or any Principal Subsidiary, as the case may be, of a lease of such Principal Property (a "Sale-Leaseback Transaction"), unless:

S-25

Notwithstanding the foregoing, EnLink Midstream may, and may permit any Principal Subsidiary to, effect any Sale-Leaseback Transaction that is not excepted by clauses (1) through (4), inclusive, of the preceding paragraph provided that the Attributable Indebtedness from such Sale-Leaseback Transaction, together with the aggregate principal amount of outstanding Indebtedness (other than the notes) secured by liens other than Permitted Liens upon Principal Properties, does not exceed 15% of Consolidated Net Tangible Assets.

Merger, Consolidation or Sale of Assets. EnLink Midstream shall not consolidate with or merge into any Person or sell, lease, convey, transfer or otherwise dispose of all or substantially all of its assets to any Person unless:

The successor will be substituted for EnLink Midstream in the indenture with the same effect as if it had been an original party to the indenture. Thereafter, the successor may exercise the rights and powers of EnLink Midstream under the indenture. If EnLink Midstream conveys or transfers all or substantially all of its assets, it will be released from all liabilities and obligations under the indenture and under the notes except that no such release will occur in the case of a lease of all or substantially all of its assets.

Defeasance and Discharge

The indenture provides that we may be:

S-26

The defeasance provisions of the indenture described in the accompanying base prospectus will apply to the notes. See "Description of the Debt Securities—Defeasance" in the accompanying base prospectus.

The indenture is also subject to discharge with respect to the notes as described in the accompanying base prospectus under "Description of the Debt Securities—Satisfaction and Discharge."

Concerning the Trustee

The indenture contains certain limitations on the right of the trustee, should it become our creditor, to obtain payment of claims in certain cases, or to realize for its own account on certain property received in respect of any such claim as security or otherwise. The trustee is permitted to engage in certain other transactions. However, if it acquires any conflicting interest within the meaning of the Trust Indenture Act after a default has occurred and is continuing, it must eliminate the conflict within 90 days, apply to the SEC for permission to continue as trustee or resign.

If an Event of Default occurs and is not cured or waived, the trustee is required to exercise such of the rights and powers vested in it by the indenture and use the same degree of care and skill in their exercise as a prudent man would exercise or use under the circumstances in the conduct of his own affairs. Subject to such provisions, the trustee will not be under any obligation to exercise any of its rights or powers under the indenture at the request of any of the holders of notes unless they have offered to the trustee reasonable security or indemnity against the costs, expenses and liabilities it may incur.

Wells Fargo Bank, National Association will be the trustee under the indenture and the registrar and paying agent with regard to the notes. The trustee and its affiliates maintain commercial banking and other relationships with EnLink Midstream.

Governing Law

The indenture and the notes will be governed by, and will be construed in accordance with, the laws of the State of New York.

Book-Entry System

We have obtained the information in this section concerning The Depository Trust Company ("DTC") and its book-entry systems and procedures from DTC, and we take no responsibility for the accuracy of this information. In addition, the description in this section reflects our understanding of the rules and procedures of DTC as they are currently in effect. DTC could change its rules and procedures at any time.

The notes will initially be represented by one or more fully registered global notes. Each such global note will be deposited with, or on behalf of, DTC or any successor thereto and registered in the name of Cede & Co. (DTC's nominee). You may hold your interests in the global notes through DTC either as a participant in DTC or indirectly through organizations that are participants in DTC.

So long as DTC or its nominee is the registered owner of the global securities representing the notes, DTC or such nominee will be considered the sole owner and holder of the notes for all purposes of the notes and the indenture. Except as provided below, owners of beneficial interests in the notes will not be entitled to have the notes registered in their names, will not receive or be entitled to receive physical delivery of the notes in definitive form and will not be considered the owners or holders of the

S-27

notes under the indenture, including for purposes of receiving any reports delivered by us or the trustee pursuant to the indenture. Accordingly, each person owning a beneficial interest in a note must rely on the procedures of DTC or its nominee and, if such person is not a participant, on the procedures of the participant through which such person owns its interest, in order to exercise any rights of a holder of notes.

The Depository Trust Company. DTC will act as securities depositary for the notes. The notes will be issued as fully registered notes registered in the name of Cede & Co. DTC has advised us as follows: DTC is

DTC holds securities that its direct participants deposit with DTC. DTC facilitates the settlement among direct participants of securities transactions, such as transfers and pledges, in deposited securities through electronic computerized book-entry changes in direct participants' accounts, thereby eliminating the need for physical movement of securities certificates.

Direct participants of DTC include securities brokers and dealers (including the underwriters), banks, trust companies, clearing corporations, and certain other organizations. DTC is owned by a number of its direct participants. Access to the DTC system is also available to securities brokers and dealers, banks and trust companies that clear through or maintain a custodial relationship with a direct participant, either directly or indirectly.

If you are not a direct participant or an indirect participant and you wish to purchase, sell or otherwise transfer ownership of, or other interests in, notes, you must do so through a direct participant or an indirect participant. DTC agrees with and represents to DTC participants that it will administer its book-entry system in accordance with its rules and by-laws and requirements of law. The SEC has on file a set of the rules applicable to DTC and its direct participants.

Purchases of notes under DTC's system must be made by or through direct participants, who will receive a credit for the notes on DTC's records. The ownership interest of each beneficial owner is in turn to be recorded on the records of direct participants and indirect participants. Beneficial owners will not receive written confirmation from DTC of their purchase, but beneficial owners are expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the direct participants or indirect participants through which such beneficial owners entered into the transaction. Transfers of ownership interests in the notes are to be accomplished by entries made on the books of participants acting on behalf of beneficial owners. Beneficial owners will not receive certificates representing their ownership interests in the notes, except in the event that use of the book-entry system for the notes is discontinued.

To facilitate subsequent transfers, all notes deposited by direct participants with DTC are registered in the name of DTC's nominee, Cede & Co., or such other name as may be requested by an authorized representative of DTC. The deposit of notes with DTC and their registration in the name of Cede & Co. do not effect any change in beneficial ownership. DTC has no knowledge of the actual beneficial owners of the notes. DTC's records reflect only the identity of the direct participants to whose accounts such notes are credited, which may or may not be the beneficial owners. The participants will remain responsible for keeping account of their holdings on behalf of their customers.

S-28

Conveyance of notices and other communications by DTC to direct participants, by direct participants to indirect participants and by direct participants and indirect participants to beneficial owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time.

Book-Entry Format. Under the book-entry format, the trustee will pay interest or principal payments to Cede & Co., as nominee of DTC. DTC will forward the payment to the direct participants, who will then forward the payment to the indirect participants or to you as the beneficial owner. You may experience some delay in receiving your payments under this system. Neither we, the trustee under the indenture nor any paying agent has any direct responsibility or liability for the payment of principal or interest on the notes to owners of beneficial interests in the notes.

DTC is required to make book-entry transfers on behalf of its direct participants and is required to receive and transmit payments of principal, premium, if any, and interest on the notes. Any direct participant or indirect participant with which you have an account is similarly required to make book-entry transfers and to receive and transmit payments with respect to the notes on your behalf. We, the underwriters and the trustee under the indenture have no responsibility for any aspect of the actions of DTC or any of its direct or indirect participants. We, the underwriters and the trustee under the indenture have no responsibility or liability for any aspect of the records kept by DTC or any of its direct or indirect participants relating to, or payments made on account of, beneficial ownership interests in the notes or for maintaining, supervising or reviewing any records relating to such beneficial ownership interests. We also do not supervise these systems in any way.