Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

TABLE OF CONTENTS

As filed with the Securities and Exchange Commission on November 4, 2002

Registration Statement No. 333-97779

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Crosstex Energy, L.P.

(Exact name of registrant as specified in its charter)

| Delaware | 4923 | 16-1616605 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

Crosstex Energy GP, L.P.

2501 Cedar Springs

Suite 600

Dallas, Texas 75201

(214) 953-9500

(Name, address, including zip code, and telephone number,

including area code, of registrant's principal executive offices)

William W. Davis

Crosstex Energy GP, L.P.

2501 Cedar Springs, Suite 600

Dallas, Texas 75201

(214) 953-9500

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

| Joshua Davidson Baker Botts L.L.P. One Shell Plaza, 910 Louisiana Houston, Texas 77002 (713) 229-1234 |

Douglass M. Rayburn Baker Botts L.L.P. 2001 Ross Avenue Dallas, Texas 75201 (214) 953-6500 |

Jeffrey A. Zlotky Thompson & Knight L.L.P. 1700 Pacific Avenue, Suite 3300 Dallas, Texas 75201 (214) 969-1700 |

David P. Oelman Melissa M. Baldwin Vinson & Elkins L.L.P. 1001 Fannin, Suite 2300 Houston, Texas 77002-6760 (713) 758-2222 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. / /

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. / /

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. / /

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. / /

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. / /

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Subject to completion, dated November 4, 2002

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS

2,000,000 Common Units

![]()

Crosstex Energy, L.P.

Representing Limited Partner Interests

We are offering 2,000,000 common units representing limited partner interests. This is the initial public offering of our common units. We expect the initial public offering price to be between $19.00 and $21.00 per common unit. Holders of common units are entitled to receive distributions of available cash of $0.50 per quarter, or $2.00 per unit on an annualized basis, before any distributions are paid on our subordinated units, to the extent we have sufficient cash from operations after establishment of cash reserves and payment of fees and expenses, including payments to our general partner. Our common units have been approved for quotation on the Nasdaq National Market under the symbol "XTEX".

Investing in our common units involves risk.

See "Risk Factors" beginning on page 15.

These risks include the following:

PRICE $ PER COMMON UNIT

| |

Per Common Unit |

Total |

||||

|---|---|---|---|---|---|---|

| Initial public offering price | $ | $ | ||||

| Underwriting discount | $ | $ | ||||

| Proceeds, before expenses, to Crosstex Energy, L.P. | $ | $ | ||||

We have granted the underwriters a 30-day option to purchase up to an additional 300,000 common units to cover over-allotments. The underwriters expect to deliver the common units to purchasers on or about , 2002.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

A.G. Edwards & Sons, Inc.

Raymond James

RBC Capital Markets

Prospectus dated , 2002

[Map showing location of gathering and transmission

systems and processing and treating facilities]

i

ii

iii

iv

v

The summary highlights selected information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the historical and pro forma financial statements and notes to those financial statements. The information presented in this prospectus assumes (1) an initial public offering price of $20.00 per common unit and (2) that the underwriters' over-allotment option is not exercised. You should read "Summary of Risk Factors" beginning on page 2 and "Risk Factors" beginning on page 15 for more information about important factors that you should consider before buying common units. We have included a "Glossary of Terms" as Appendix C that defines many of the terms we use in this prospectus.

References in this prospectus to "Crosstex Energy, L.P.," "we," "ours," "us," or like terms when used in the present tense or prospectively refer to Crosstex Energy, L.P. and its operating subsidiaries. Crosstex Energy, L.P. is the issuer of securities in this offering. References to "our predecessor," "we," "ours," "us," or like terms when used in a historical context refer to Crosstex Energy Services, Ltd. Substantially all of the assets of Crosstex Energy Services, Ltd. will be transferred to us at the closing of the offering.

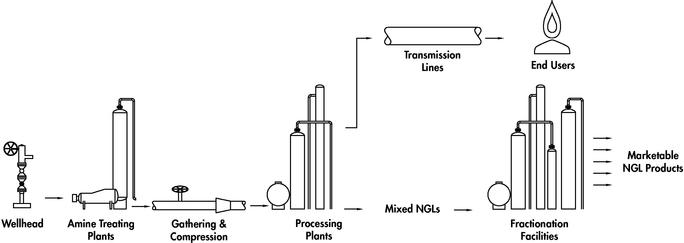

We are a rapidly growing independent midstream energy company engaged in the gathering, transmission, treating, processing and marketing of natural gas. We connect the wells of natural gas producers in our market areas to our gathering systems, treat natural gas to remove impurities to ensure that it meets pipeline quality specifications, process natural gas for the removal of natural gas liquids, or NGLs, transport natural gas and ultimately provide an aggregated supply of natural gas to a variety of markets. We purchase natural gas from natural gas producers and other supply points and sell that natural gas to utilities, industrial consumers, other marketers and pipelines and thereby generate gross margins based on the difference between the purchase and resale prices. In addition, we purchase natural gas from producers not connected to our gathering systems for resale and sell natural gas on behalf of producers for a fee.

We have grown rapidly since the inception of our various predecessors in 1992 through a combination of acquisitions and the construction of new assets. Our income before income taxes plus depreciation and amortization expense and interest expense, which we refer to as EBITDA, has increased from $0.5 million in 1997 to $4.4 million in 2001. Our EBITDA was $9.9 million for the nine months ended September 30, 2002. Our net loss was $3.9 million for the year ended December 31, 2001, and net income was $1.5 million for the nine months ended September 30, 2002. Net income and EBITDA for 2001 and the nine months ended September 30, 2002 have been reduced by non-cash impairment charges of $2.9 million and $3.2 million, respectively.

We have two operating divisions, the Midstream division, which consists of our natural gas gathering, transmission, processing, marketing and producer services operations, and the Treating division, which provides natural gas treating for the removal of carbon dioxide and other contaminants.

Midstream Division

Our primary Midstream assets are four major systems along the Texas Gulf Coast and one in eastern Oklahoma, which in the aggregate consist of approximately 1,500 miles of gathering and transmission pipelines, and a natural gas processing plant connected to one of these gathering systems. For the nine months ended September 30, 2002, we gathered and transported approximately 368,681 Mcf/d of natural gas.

1

Texas to Fort Bend County near Houston, Texas. Our Gulf Coast system had an average throughput of approximately 101,021 Mcf/d for the nine months ended September 30, 2002.

In our producer services operations, we purchase for resale volumes of natural gas that do not move through our gathering, processing or transmission assets from over 80 independent producers. We focus on supply aggregation transactions in which we either purchase and resell gas and thereby eliminate the need of the producer to engage in the marketing activities typically handled by in-house marketing or supply departments of larger companies, or act as agent for the producer.

Treating Division

Our treating plants remove carbon dioxide and hydrogen sulfide from natural gas before it is delivered into transportation systems to ensure that the natural gas meets pipeline quality specifications. As of September 30, 2002, we owned 49 mobile, skid-mounted treating plants of various sizes, 23 of which were operated by our personnel, six of which were operated by producers, one of which was operated by a joint venture partner and 19 of which were held in inventory.

An investment in our common units involves risks associated with our business, our partnership structure and the tax characteristics of common units. Those risks are described under the caption "Risk Factors" and include:

Risks Inherent in Our Business

2

Risks Inherent in an Investment in Us

3

Tax Risks to Our Unitholders

We believe that we are well positioned to compete in the natural gas gathering, transmission, treating, processing and producer services businesses. Our competitive strengths include:

Our treating operations, with 19 treating plants of varying sizes available in inventory, provides us with an advantageous position to compete for new treating business in the Texas Gulf Coast because natural gas produced from certain deeper formations in the Texas Gulf Coast is high in carbon dioxide. We believe our inventory of available treating plants gives us a competitive advantage for new treating business since we can often have a plant in service quicker than our competitors.

4

provide us with a flexible financial structure that will facilitate our strategic expansion and acquisition strategy.

Our strategy is to increase distributable cash flow per unit by improving the profitability of our existing systems through increasing volumes and reducing costs, focusing on accretive acquisitions and pursuing system construction and expansion opportunities. Key elements of our strategy include the following:

5

PARTNERSHIP STRUCTURE AND MANAGEMENT

Our operations will be conducted through, and our operating assets will be owned by, our operating partnership, Crosstex Energy Services, L.P., and its subsidiaries. Our general partner, Crosstex Energy GP, L.P., has sole responsibility for conducting our business and for managing our operations. The senior executives who currently manage our business will continue to manage and operate the business as the senior executives of Crosstex Energy GP, LLC, the general partner of our general partner. Our general partner will not receive any management fee or other compensation in connection with its management of our business but will be entitled to reimbursement for all direct and indirect expenses incurred on our behalf. Upon completion of this offering and the related transactions:

We are using a limited partnership, Crosstex Energy GP, L.P., as our general partner instead of Crosstex Energy Holdings Inc. primarily to limit the liability of Crosstex Energy Holdings Inc. and its institutional holders. Crosstex Energy Services GP, LLC is inserted between us and our operating partnership to serve as the general partner of the operating partnership. In the event that our operating partnership ever issues public debt securities, having the operating partnership and all subsidiary guarantors 100% owned by us will allow the use of condensed financial information for the operating partnership and guarantors instead of separate financial statements. We have no current plans for our operating partnership to issue public debt.

Our principal executive offices are located at 2501 Cedar Springs, Suite 600, Dallas, Texas 75201, and our phone number is (214) 953-9500.

The chart on the following page depicts the organization and ownership of us and our operating partnership after giving effect to the offering and the related formation transactions.

6

7

| Common units offered to the public | 2,000,000 common units. | |||

2,300,000 common units if the underwriters exercise their over-allotment option in full. |

||||

Units outstanding after this offering |

2,333,000 common units, representing a 32.7% limited partner interest in Crosstex Energy, L.P., and 4,667,000 subordinated units, representing a 65.3% limited partner interest in Crosstex Energy, L.P. Approximately 14.3% of the common units and all of the subordinated units will be owned by affiliates of our general partner. |

|||

Cash distributions |

We intend to make minimum quarterly distributions of $0.50 per common unit to the extent we have sufficient cash from our operations after establishment of cash reserves and payment of fees and expenses, including payments to our general partner. In general, we will pay any cash distributions we make each quarter in the following manner: |

|||

• |

first, 98% to the common units and 2% to the general partner, until each common unit has received a minimum quarterly distribution of $0.50 plus any arrearages from prior quarters; and |

|||

• |

second, 98% to the subordinated units and 2% to the general partner, until each subordinated unit has received a minimum quarterly distribution of $0.50. |

|||

If cash distributions exceed $0.50 per unit in a quarter, our general partner will receive increasing percentages, up to 50%, of the cash we distribute in excess of that amount. We refer to these distributions as "incentive distributions." Please read "Cash Distribution Policy—Incentive Distribution Rights." |

||||

We must distribute all of our cash on hand at the end of each quarter, less reserves established by our general partner in its sole discretion. These reserve funds are meant to provide for the proper conduct of our business including funds needed to provide for our operations as well as to comply with applicable debt instruments. As we cannot estimate the size of these reserves for any given quarter at this time, we cannot assure you that, after the establishment of reserves, we will have cash on hand for distribution to our unitholders. We refer to this cash available for distribution as "available cash," and we define its meaning in our partnership agreement. Please read "Cash Distribution Policy—Distributions of Available Cash" for a description of available cash. The amount of available cash may be greater than or less than the minimum quarterly distribution. |

||||

8

We believe, based on the forecast included in Appendix E and the assumptions described therein, that we will have sufficient cash from operations to enable us to make the minimum quarterly distribution of $0.50 on all of the common units and the subordinated units for each quarter through September 30, 2003. The amount of pro forma cash available for distribution generated during 2001 and the first nine months of 2002 would have been sufficient to allow us to pay the minimum quarterly distribution on all of the common units and 5.5% and 78.7%, respectively, of the minimum quarterly distribution on the subordinated units during these periods. Please read "Cash Available for Distribution." |

||||

Subordination period |

The subordination period will end once we meet the financial tests in the partnership agreement, but it generally cannot end before December 31, 2007. |

|||

When the subordination period ends, each remaining subordinated unit will convert into one common unit and the common units will no longer be entitled to arrearages. Please read "Cash Distribution Policy—Subordination Period." |

||||

Early conversion of subordinated units |

If we meet the applicable financial tests in the partnership agreement for any three consecutive four-quarter periods ending on or after December 31, 2005, 25% of the subordinated units will convert into common units. If we meet these tests for any three consecutive four-quarter periods ending on or after December 31, 2006, an additional 25% of the subordinated units will convert into common units. The early conversion of the second 25% of the subordinated units may not occur until at least one year after the early conversion of the first 25% of the subordinated units. |

|||

Issuance of additional units |

In general, while any subordinated units remain outstanding, we may not issue more than 1,166,500 additional common units, or 50% of the common units outstanding immediately after this offering, without obtaining unitholder approval. We may, however, issue an unlimited number of common units for acquisitions, capital improvements or debt repayments that increase cash flow from operations per unit on a pro forma basis. |

|||

Voting rights |

Our general partner will manage and operate us. Unlike the holders of common stock in a corporation, you will have only limited voting rights on matters affecting our business. You will have no right to elect our general partner or the directors of its general partner on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 662/3% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Because affiliates of our general partner will own 71.4% of the outstanding units upon completion of the offering, you will not be able to remove the general partner without its consent. |

|||

9

Limited call right |

If at any time more than 80% of the outstanding common units are owned by our general partner and its affiliates, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price not less than the then-current market price of the common units. At the end of the subordination period, assuming no additional issuances of common units, our general partner and its affiliates will own 71.4% of the common units. |

|||

Estimated ratio of taxable income to distributions |

We estimate that if you own the common units you purchase in this offering through December 31, 2005, you will be allocated, on a cumulative basis, an amount of federal taxable income for that period that will be 20% or less of the cash distributed to you with respect to that period. Please read "Material Tax Consequences—Tax Consequences of Unit Ownership—Ratio of taxable income to distributions" for the basis of this estimate. |

|||

Exchange listing |

Our common units have been approved for quotation on the Nasdaq National Market under the symbol "XTEX". |

|||

10

SUMMARY HISTORICAL AND PRO FORMA FINANCIAL AND OPERATING DATA

The following table sets forth summary historical financial and operating data of our predecessor, Crosstex Energy Services, Ltd., as of and for the dates and periods indicated and the summary pro forma financial and operating data of Crosstex Energy, L.P. as of and for the year ended December 31, 2001 and the nine months ended September 30, 2002. The summary historical financial data for the years ended December 31, 1999 and 2001 and for the four months ended April 30, 2000 and for the eight months ended December 31, 2000 are derived from the audited financial statements of Crosstex Energy Services, Ltd. and its predecessor. The summary historical financial data for the nine months ended September 30, 2001 and 2002 are derived from the unaudited financial statements of Crosstex Energy Services, Ltd. and, in our opinion, have been prepared on the same basis as the audited financial statements and include all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of this information. As described in our historical financial statements, the investment in our predecessor by Yorktown Energy Partners IV, L.P. in May 2000 resulted in the dissolution of the predecessor partnership and the creation of a new partnership with the same organization, purpose, assets, and liabilities. Accordingly, the audited financial statements of our predecessor for 2000 are divided into the four months ended April 30, 2000 and the eight months ended December 31, 2000 because a new basis of accounting was established effective May 1, 2000 to give effect to the Yorktown transaction. In addition, the summary historical financial and operating data of Crosstex Energy Services, Ltd. include the results of operations of the Arkoma system beginning in September 2000, the Gulf Coast system beginning in September 2000 and the CCNG system, which includes the Corpus Christi system, the Gregory gathering system and the Gregory processing plant, beginning in May 2001.

The summary pro forma financial and operating data of Crosstex Energy, L.P. reflect the consolidated historical operating results of Crosstex Energy Services, Ltd., as adjusted for the offering and the related transactions. The summary pro forma financial data are derived from the unaudited pro forma financial statements. The pro forma balance sheet assumes that the offering and related transactions occurred on September 30, 2002. The pro forma statements of operations assume that the offering and related transactions occurred on January 1, 2001. For a description of all of the assumptions used in preparing the summary pro forma financial data, you should read the notes to the pro forma financial statements for Crosstex Energy, L.P. The pro forma financial and operating data should not be considered as indicative of the historical results we would have had or the future results that we will have after the offering.

We define EBITDA as income (loss) before income taxes plus depreciation and amortization expense and interest expense. As described in the following paragraph, we use EBITDA as a supplemental measurement to evaluate our business. We also understand that such data is used by investors to determine our historical ability to service our indebtedness and make cash distributions to unitholders. However, the term EBITDA is not defined under generally accepted accounting principles and EBITDA is not a measurement of operating income, operating performance or liquidity presented in accordance with generally accepted accounting principles. You should not consider this data in isolation or as a substitute to net income as an indicator of our operating performance, cash flows from operating activities or other cash flow data calculated in accordance with generally accepted accounting principles. You should also not consider EBITDA as a measure of liquidity. Our EBITDA may not be comparable to EBITDA or similarly titled measures of other entities as other entities may not calculate EBITDA in the same manner as we do.

We use EBITDA as a supplemental financial measure to assess:

11

Consequently, we use this supplemental financial measure when assessing liquidity and performance over time, and in comparison to companies that own similar assets and that our management believes calculate EBITDA in a manner similar to us. Although we use EBITDA to assess our ability to generate cash sufficient to pay interest costs and make cash distributions to our unitholders, the amount of cash available for such payments may be subject to our ability to reserve cash for other uses, such as debt repayments, capital expenditures and operating activities.

Maintenance capital expenditures are capital expenditures made to replace partially or fully depreciated assets in order to maintain the existing operating capacity of our assets and to extend their useful lives. Expansion capital expenditures are capital expenditures made to expand the existing operating capacity of our assets, whether through construction or acquisition. We treat repair and maintenance expenditures that do not extend the useful life of existing assets as operating expenses as we incur them.

We derived the information in the following table from, and that information should be read together with, and is qualified in its entirety by reference to, the historical and pro forma financial statements and the accompanying notes included in this prospectus. The table should be read together with "Management's Discussion and Analysis of Financial Condition and Results of Operations."

12

| |

Crosstex Energy Services, Ltd. — Historical(1) |

|

|

|||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Predecessor |

|

|

|

|

Crosstex Energy, L.P. Pro Forma |

||||||||||||||||||||||

| |

Successor |

|||||||||||||||||||||||||||

| |

|

Four Months Ended April 30, |

||||||||||||||||||||||||||

| |

Year Ended December 31, |

Eight Months Ended December 31, |

Year Ended December 31, |

Nine Months Ended September 30, |

Year Ended December 31, |

Nine Months Ended September 30, |

||||||||||||||||||||||

| |

1999 |

2000 |

2000 |

2001 |

2001 |

2002 |

2001 |

2002 |

||||||||||||||||||||

| |

(in thousands, except per unit amounts and operating data) |

|||||||||||||||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||||||||

| Midstream | $ | 7,896 | $ | 3,591 | $ | 88,008 | $ | 362,673 | $ | 270,496 | $ | 311,453 | $ | 362,340 | $ | 311,279 | ||||||||||||

| Treating | 9,770 | 5,947 | 17,392 | 24,353 | 19,084 | 10,631 | 24,353 | 10,631 | ||||||||||||||||||||

| Total revenues | 17,666 | 9,538 | 105,400 | 387,026 | 289,580 | 322,084 | 386,693 | 321,910 | ||||||||||||||||||||

| Operating costs and expenses: | ||||||||||||||||||||||||||||

| Midstream purchased gas | 5,154 | 2,746 | 83,672 | 344,755 | 258,670 | 294,025 | 344,493 | 293,916 | ||||||||||||||||||||

| Treating purchased gas | 8,110 | 4,731 | 14,876 | 18,078 | 14,854 | 3,996 | 18,078 | 3,996 | ||||||||||||||||||||

| Operating expenses | 986 | 544 | 1,796 | 7,430 | 4,995 | 7,732 | 7,313 | 7,643 | ||||||||||||||||||||

| General and administrative | 2,078 | 810 | 2,010 | 5,914 | 4,367 | 6,247 | 5,914 | 4,500 | ||||||||||||||||||||

| Stock based compensation | — | 8,802 | — | — | — | 33 | — | 33 | ||||||||||||||||||||

| Impairments | 538 | — | — | 2,873 | — | 3,150 | — | 3,150 | ||||||||||||||||||||

| (Profit) loss on energy trading contracts | (1,764 | ) | (638 | ) | (1,253 | ) | 3,714 | (1,527 | ) | (2,916 | ) | 3,714 | (2,916 | ) | ||||||||||||||

| Depreciation and amortization | 1,286 | 522 | 2,261 | 6,101 | 4,181 | 6,034 | 5,802 | 5,884 | ||||||||||||||||||||

| Total operating costs and expenses | 16,388 | 17,517 | 103,362 | 388,865 | 285,540 | 318,301 | 385,314 | 316,206 | ||||||||||||||||||||

| Operating income (loss) | 1,278 | (7,979 | ) | 2,038 | (1,839 | ) | 4,040 | 3,783 | 1,379 | 5,704 | ||||||||||||||||||

| Other income (expense): | ||||||||||||||||||||||||||||

| Interest expense, net | (638 | ) | (79 | ) | (530 | ) | (2,253 | ) | (1,538 | ) | (2,399 | ) | (147 | ) | (1,204 | ) | ||||||||||||

| Other income (expense) | (138 | ) | 381 | 115 | 174 | 145 | 73 | 174 | 73 | |||||||||||||||||||

| Total other income (expense) | (776 | ) | 302 | (415 | ) | (2,079 | ) | (1,393 | ) | (2,326 | ) | 27 | (1,131 | ) | ||||||||||||||

| Net income (loss) | $ | 502 | $ | (7,677 | ) | $ | 1,623 | $ | (3,918 | ) | $ | 2,647 | $ | 1,457 | $ | 1,406 | $ | 4,573 | ||||||||||

| Pro forma net income per limited partner unit | $ | 0.20 | $ | 0.64 | ||||||||||||||||||||||||

| Balance Sheet Data (at period end): | ||||||||||||||||||||||||||||

| Working capital surplus (deficit) | $ | (3,483 | ) | $ | (4,005 | ) | $ | 5,861 | $ | (2,254 | ) | $ | (2,446 | ) | $ | (8,598 | ) | $ | (8,598 | ) | ||||||||

| Property and equipment, net | 8,072 | 10,540 | 37,242 | 84,951 | 81,524 | 92,443 | 91,143 | |||||||||||||||||||||

| Total assets | 36,497 | 45,051 | 201,268 | 168,376 | 154,216 | 214,862 | 211,095 | |||||||||||||||||||||

| Long-term debt | 5,389 | 7,000 | 22,000 | 60,000 | 49,500 | 43,250 | 11,050 | |||||||||||||||||||||

| Partners' equity | 3,242 | 3,608 | 40,354 | 41,155 | 47,804 | 55,820 | 84,253 | |||||||||||||||||||||

| Cash Flow Data: | ||||||||||||||||||||||||||||

| Net cash flow provided by (used in): | ||||||||||||||||||||||||||||

| Operating activities | $ | 1,404 | $ | 7,380 | $ | 7,741 | $ | (8,326 | ) | $ | 10,397 | $ | 15,087 | |||||||||||||||

| Investing activities | (1,342 | ) | (2,849 | ) | (25,643 | ) | (52,535 | ) | (47,255 | ) | (12,689 | ) | ||||||||||||||||

| Financing activities | (857 | ) | 198 | 36,557 | 42,558 | 32,200 | (2,750 | ) | ||||||||||||||||||||

| Other Financial Data: | ||||||||||||||||||||||||||||

| EBITDA(2) | $ | 2,426 | $ | (7,076 | ) | $ | 4,414 | $ | 4,436 | $ | 8,366 | $ | 9,890 | $ | 7,355 | $ | 11,661 | |||||||||||

| Maintenance capital expenditures | 57 | 1,922 | 1,228 | 1,267 | 1,922 | 1,267 | ||||||||||||||||||||||

| Expansion capital expenditures | 25,743 | 50,766 | 46,116 | 11,509 | 50,766 | 11,509 | ||||||||||||||||||||||

| Total capital expenditures | $ | 25,800 | $ | 52,688 | $ | 47,344 | $ | 12,776 | $ | 52,688 | $ | 12,776 | ||||||||||||||||

| Operating Data: | ||||||||||||||||||||||||||||

| Pipeline throughput (MMBtu/d) | 19,712 | 23,098 | 104,185 | 313,103 | 290,591 | 393,261 | 313,103 | 393,261 | ||||||||||||||||||||

| Natural gas processed (MMBtu/d) | 23,112 | 30,699 | 15,661 | 60,629 | 47,776 | 86,753 | 57,775 | 84,136 | ||||||||||||||||||||

| Treating volumes (MMBtu/d)(3) | 12,896 | 26,872 | 35,910 | 62,782 | 57,663 | 98,039 | 62,782 | 98,039 | ||||||||||||||||||||

13

SUMMARY OF CONFLICTS OF INTEREST AND FIDUCIARY RESPONSIBILITIES

Crosstex Energy GP, L.P., our general partner, has a legal duty to manage us in a manner beneficial to our unitholders. This legal duty originates in statutes and judicial decisions and is commonly referred to as a "fiduciary" duty. However, because Crosstex Energy GP, L.P. is indirectly owned by Crosstex Energy Holdings Inc., the officers and directors of Crosstex Energy GP, LLC, who manage and operate our general partner, have fiduciary duties to manage the business of our general partner in a manner beneficial to Crosstex Energy Holdings Inc. The officers and directors of Crosstex Energy GP, LLC have significant relationships with, and responsibilities to, Crosstex Energy Holdings Inc. As a result of this relationship, conflicts of interest may arise in the future between us and our unitholders, on the one hand, and our general partner and its affiliates, on the other hand. For a more detailed description of the conflicts of interest and fiduciary responsibilities of our general partner, please read "Conflicts of Interest and Fiduciary Responsibilities."

Our general partner is permitted to resolve conflicts of interest by considering the interests of all the parties involved. Therefore, our general partner can consider the interests of its affiliates if a conflict of interest arises between the common unitholders and our general partner and its affiliates. Crosstex Energy GP, LLC will have a conflicts committee, consisting of at least two independent members of its board of directors, that will be available to review matters involving conflicts of interest. We expect that C. Roland Haden, Stephen A. Wells and Robert F. Murchison, all of whom will become directors of Crosstex Energy GP, LLC upon completion of this offering, will be members of the conflicts committee. Please read "Management—Directors and Executive Officers of Crosstex Energy GP, LLC" for a discussion of the directors of Crosstex Energy GP, LLC.

Our partnership agreement limits the liability and reduces the fiduciary duties owed by our general partner to the unitholders. Our partnership agreement also restricts the remedies available to unitholders for actions that might otherwise constitute breaches of our general partner's fiduciary duty. By purchasing a common unit, you are treated as having consented to various actions contemplated in the partnership agreement and conflicts of interest that might otherwise be considered a breach of fiduciary or other duties under applicable state law.

We will enter into an agreement with Crosstex Energy Holdings Inc. whereby it will generally agree not to engage in the business of gathering, transmitting, treating, processing and marketing of natural gas. In addition, our general partner will not receive any management fee or other compensation for its management of us but our general partner and its affiliates will be reimbursed for general and administrative expenses incurred on our behalf. For the twelve months following this offering, the amount which we will reimburse the general partner and its affiliates for costs incurred with respect to the general and administrative services performed on our behalf will not exceed $6.0 million. For a more detailed discussion of these agreements, please read "Certain Relationships and Related Transactions."

14

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors, which we believe include the risks material to our business, together with all of the other information included in this prospectus in evaluating an investment in the common units.

If any of the following risks were actually to occur, our business, financial condition, or results of operations could be materially adversely affected. In that case, we might not be able to pay distributions on our common units, the trading price of our common units could decline and you could lose all or part of your investment.

Risks Inherent in Our Business

We may not have sufficient cash after the establishment of cash reserves and payment of our general partner's fees and expenses to enable us to pay the minimum quarterly distribution each

quarter.

We may not have sufficient available cash each quarter to pay the minimum quarterly distribution. Under the terms of our partnership agreement, we must pay our general partner's fees and expenses and set aside any cash reserve amounts before making a distribution to our unitholders. The amount of cash we can distribute on our common units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things;

In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including:

Because of these factors, we may not have sufficient available cash each quarter to pay the minimum quarterly distribution. Furthermore, you should also be aware that the amount of cash we have available for distribution depends primarily upon our cash flow, including cash flow from financial

15

reserves and working capital borrowings, and is not solely a function of profitability, which will be affected by non-cash items. As a result, we may make cash distributions during periods when we record losses and may not make cash distributions during periods when we record net income.

The amount of available cash we need to pay the minimum quarterly distribution for four quarters on the common units, the subordinated units and the general partner interest to be outstanding immediately after the offering is approximately $14.3 million. If we had completed the transactions contemplated in this prospectus on January 1, 2001, pro forma available cash from operating surplus generated during the year ended December 31, 2001 would have been approximately $5.3 million. If we had completed the transactions contemplated in this prospectus on January 1, 2002, pro forma available cash from operating surplus generated during the nine months ended September 30, 2002 would have been approximately $9.2 million. The amount of pro forma cash available for distribution during 2001 and the first nine months of 2002 would have been sufficient to allow us to pay the minimum quarterly distribution on all the common units and 5.5% and 78.7%, respectively, of the minimum quarterly distribution on the subordinated units during these periods. For a calculation of our ability to make distributions to you based on our pro forma results for the year ended December 31, 2001 and for the nine months ended September 30, 2002, please read "Cash Available for Distribution" and Appendix D.

The assumptions underlying the financial forecast in Appendix E are inherently uncertain and are subject to significant business, economic, regulatory and competitive risks and uncertainties that could cause actual

results to differ materially from those forecasted.

The financial forecast set forth in Appendix E includes our forecast of statements of operations for the twelve months ending September 30, 2003. The financial forecast has been prepared by management and we have not received an opinion or report on it from any independent accountants. In addition, Appendix E includes a calculation of available cash from operating surplus based on the financial forecast. The assumptions underlying the financial forecast are inherently uncertain and are subject to significant business, economic, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those forecasted. If the forecasted results are not achieved, we may not be able to pay the full minimum quarterly distributions or any amount on the common units or subordinated units, in which event the market price of the common units may decline materially.

We must continually compete for natural gas supplies, and any decrease in our supplies of natural gas could reduce our ability to make distributions to our unitholders.

Competition is intense in many of our markets. The principal areas of competition include obtaining gas supplies and the marketing and transportation of natural gas and NGLs. Our competitors include major integrated oil companies, interstate and intrastate pipelines and natural gas gatherers and processors. Our competitors in the Texas Gulf Coast area include El Paso Field Services, Kinder Morgan Inc., Houston Pipeline Company and Duke Energy Field Services. Some of our competitors offer more services or have greater financial resources and access to larger natural gas supplies than we do.

If we are unable to maintain or increase the throughput on our systems by accessing new natural gas supplies to offset the natural decline in reserves, our business and financial results could be materially adversely affected. In addition, our future growth will depend, in part, upon whether we can contract for additional supplies at a greater rate than the rate of natural decline in our currently connected supplies.

In order to maintain or increase throughput levels in our natural gas gathering systems and asset utilization rates at our treating and processing plants, we must continually contract for new natural gas

16

supplies. We may not be able to obtain additional contracts for natural gas supplies. The primary factors affecting our ability to connect new wells to our gathering facilities include our success in contracting for existing natural gas supplies that are not committed to other systems and the level of drilling activity near our gathering systems. Fluctuations in energy prices can greatly affect production rates and investments by third parties in the development of new oil and natural gas reserves. Drilling activity generally decreases as oil and natural gas prices decrease. We have no control over producers and depend on them to maintain sufficient levels of drilling activity. A material decrease in natural gas production for a prolonged period along the Texas Gulf Coast, as a result of depressed commodity prices or otherwise, likely would have a material adverse effect on our results of operations and financial position. See "Business—Natural Gas Supply" for more information on our supplies of natural gas.

A substantial portion of our assets are connected to natural gas reserves that will decline over time, and the cash flows associated with those assets will accordingly decline.

A substantial portion of our assets, including our gathering systems and our treating plants, are dedicated to certain natural gas reserves and wells for which the production will naturally decline over time. Accordingly, our cash flows associated with these assets will also decline. If we are unable to access new supplies of natural gas either by connecting additional reserves to our existing assets or by constructing or acquiring new assets that have access to additional natural gas reserves, our ability to make distributions to our unitholders could decrease.

Our profitability is dependent upon prices and market demand for natural gas and NGLs, which are beyond our control and have been volatile.

We are subject to significant risks due to fluctuations in commodity prices. These risks are based upon two components of our business: (1) the purchase of certain volumes of natural gas at a price that is a percentage of a relevant index; and (2) certain processing contracts for our Gregory system whereby we are exposed to natural gas and NGL commodity price risks.

The margins we realize from purchasing and selling a portion of the natural gas that we transport through our pipeline systems decrease in periods of low natural gas prices because our gross margins are based on a percentage of the index price. For the nine months ended September 30, 2002, we purchased approximately 6.5% of our gas at a percentage of relevant index. Accordingly, a decline in the price of natural gas could have an adverse impact on our results of operations.

A portion of our profitability is affected by the relationship between natural gas and NGL prices. For a component of our Gregory system volumes, we purchase natural gas, process natural gas and extract NGLs, and then sell the processed natural gas and NGLs. Since we extract Btus from the gas stream in the form of the liquids or consume it as fuel during processing, we reduce the Btu content of the natural gas. Accordingly, our margins under these arrangements can be negatively affected in periods in which the value of natural gas is high relative to the value of NGLs. For example, a decrease of $.01 per gallon in the price of NGLs and an increase of $0.10 per MMBtu in the average price of natural gas for the nine months ended September 30, 2002 would have resulted in decreases in processing margins of approximately $341,600. For the nine months ended September 30, 2002, we purchased approximately 44% of the natural gas volumes on our Gregory system under such contracts.

In the past, the prices of natural gas and NGLs have been extremely volatile and we expect this volatility to continue. For example, in 2001, the NYMEX settlement price for the prompt month contract ranged from a high of $9.98 per MMBtu to a low of $1.83 per MMBtu. In the first nine months of 2002, the same index ranged from $3.47 per MMBtu to $2.01 per MMBtu. A composite of the OPIS Mt. Belvieu monthly average liquids price based upon our average liquids composition in 2001 ranged from a high of approximately $0.71 per gallon to a low of approximately $0.27 per gallon.

17

In the first nine months of 2002, the same composite ranged from approximately $0.44 per gallon to approximately $0.27 per gallon.

We may not be successful in balancing our purchases and sales. In addition, a producer could fail to deliver promised volumes or deliver in excess of contracted volumes, or a consumer could purchase less than contracted volumes. Any of these actions could cause our purchases and sales not to be balanced. If our purchases and sales are not balanced, we will face increased exposure to commodity price risks and could have increased volatility in our operating income.

The markets and prices for residue gas and NGLs depend upon factors beyond our control. These factors include demand for oil, natural gas and NGLs, which fluctuate with changes in market and economic conditions and other factors, including:

We are exposed to the credit risk of our customers, and a general increase in the nonpayment and nonperformance by our customers could reduce our ability to make distributions to our unitholders.

Risks of nonpayment and nonperformance by our customers are a major concern in our business. Several of our customers have been receiving heightened scrutiny from the financial markets in light of the collapse of Enron Corp. We are subject to risks of loss resulting from nonpayment or nonperformance by these and other customers. We recognized a charge of $5.7 million in 2001 for sales contracts with Enron. These contracts related to our producer services operations in which we purchased and sold natural gas that did not move on our gathering and transmission systems. Any increase in the nonpayment and nonperformance by our customers could reduce our ability to make distributions to our unitholders.

We may not be able to retain existing customers or acquire new customers, which would reduce our revenues and limit our future profitability.

The renewal or replacement of existing contracts with our customers at rates sufficient to maintain current revenues and cash flows depends on a number of factors beyond our control, including competition from other pipelines, and the price of, and demand for, natural gas in the markets we serve.

For the nine months ended September 30, 2002, approximately 63% of our sales of gas which were transported using our physical facilities were to industrial end-users and utilities. As a consequence of the increase in competition in the industry and volatility of natural gas prices, end-users and utilities are reluctant to enter into long-term purchase contracts. Many end-users purchase natural gas from more than one natural gas company and have the ability to change providers at any time. Some of these end-users also have the ability to switch between gas and alternate fuels in response to relative price fluctuations in the market. Because there are numerous companies of greatly varying size and financial capacity that compete with us in the marketing of natural gas, we often compete in the

18

end-user and utilities markets primarily on the basis of price. The inability of our management to renew or replace our current contracts as they expire and to respond appropriately to changing market conditions could have a negative effect on our profitability.

We depend on certain key customers, and the loss of any of our key customers could adversely affect our financial results.

We currently derive a significant portion of our revenues from contracts with a subsidiary of Kinder Morgan Inc., and we have entered into gas sales contracts with Entex Gas Resources, the local gas distribution company for the city of Houston, which commenced July 1, 2002. To the extent that these and other customers may reduce volumes of natural gas purchased under existing contracts, we would be adversely affected unless we were able to make comparably profitable arrangements with other customers. Sales to the subsidiary of Kinder Morgan accounted for 28.2% of our revenues during the first nine months of 2002 and 23.9% of our revenues during 2001. Our agreements with our key customers provide for minimum volumes of natural gas that each customer must purchase until the expiration of the term of the applicable agreement, subject to certain force majeure provisions. Our customers may default on their obligations to purchase the minimum volumes required under the applicable agreements. Our primary contract with Kinder Morgan expires in March 2006 and our contract with Entex expires in July 2004.

Our rapid growth may cause difficulties integrating new operations, and we have a limited combined operating history.

Since January 2000, we have made 10 acquisitions with an aggregate purchase price of approximately $60.6 million that have significantly increased our asset base. Unexpected costs or challenges may arise whenever different operations are combined. Any acquisition involves potential integration risks, including:

If we are unable to successfully integrate the companies, businesses or assets that we have acquired or in the future may acquire, our revenues may decline and we could, therefore, experience a material adverse effect on our business, financial condition or results of operations.

As a result of our rapid growth, our long-term debt has increased from approximately $3.6 million at December 31, 1997 to $43.3 million at September 30, 2002, an increase of approximately 1,100%.

Because we have grown rapidly, we have a limited operating history for most of our operations to which you may look to evaluate our performance. As a result, the historical and pro forma information may not give you an accurate indication of what our actual results would have been if the acquisitions had been completed at the beginning of the periods presented or of what our future results of operations are likely to be.

Growing our business by constructing new pipelines and processing and treating facilities subjects us to construction risks and risks that natural gas supplies will not be available upon completion of the facilities.

One of the ways we intend to grow our business is through the construction of additions to our existing gathering systems and construction of new processing and treating facilities. We have no material commitments for expansion projects as of the date of this prospectus. However, we are

19

currently studying the possibility of expanding the capacity of our Gregory processing plant by 65,000 Mcf/d at an estimated cost ranging from $6.5 million to $9.1 million. The construction of gathering, processing and treating facilities requires the expenditure of significant amounts of capital, which may exceed our expectations. Generally, we may have only limited natural gas supplies committed to these facilities prior to their construction. Moreover, we may construct facilities to capture anticipated future growth in production in a region in which anticipated production growth does not materialize. We may also rely on estimates of proved reserves in our decision to construct new pipelines and facilities, which may prove to be inaccurate because there are numerous uncertainties inherent in estimating quantities of proved reserves. As a result, new facilities may not be able to attract enough natural gas to achieve our expected investment return, which could adversely affect our results of operations and financial condition.

Our business involves many hazards and operational risks, some of which may not be fully covered by insurance.

Our operations are subject to the many hazards inherent in the gathering, compressing, treating and processing of natural gas and storage of residue gas, including:

These risks could result in substantial losses due to personal injury and/or loss of life, severe damage to and destruction of property and equipment and pollution or other environmental damage and may result in curtailment or suspension of our related operations. Our operations are concentrated in the Texas Gulf Coast, and a natural disaster or other hazard affecting this region could have a material adverse effect on our operations. We are not fully insured against all risks incident to our business. In accordance with typical industry practice, we do not have any property insurance on any of our underground pipeline systems which would cover damage to the pipelines. We are not insured against all environmental accidents which might occur, other than those considered to be sudden and accidental. Our business interruption insurance covers only our Gregory processing plant. If a significant accident or event occurs that is not fully insured, it could adversely affect our operations and financial condition.

Terrorist attacks, such as the attacks that occurred on September 11, 2001, have resulted in increased costs, and future war or risk of war may adversely impact our results of operations.

The impact that the terrorist attacks of September 11, 2001 may have on the energy industry in general, and on us in particular, is not known at this time. Uncertainty surrounding retaliatory military strikes or a sustained military campaign may affect our operations in unpredictable ways, including disruptions of fuel supplies and markets, and the possibility that infrastructure facilities, including pipelines, production facilities, and transmission and distribution facilities, could be direct targets, or indirect casualties, of an act of terror.

The terrorist attacks on September 11, 2001 and the changes in the insurance markets attributable to the September 11 attacks have made certain types of insurance more difficult for us to obtain. Our insurance policies now generally exclude acts of terrorism as compared to our policies prior to September 11, 2001. Such insurance is not available at what we believe to be acceptable pricing levels. A lower level of economic activity could also result in a decline in energy consumption, which could

20

adversely affect our revenues or restrict our future growth. Instability in the financial markets as a result of terrorism or war could also affect our ability to raise capital.

Our indebtedness may limit our ability to borrow additional funds, make distributions to you or capitalize on acquisitions or other business opportunities.

As of September 30, 2002, our total long-term indebtedness was approximately $43.3 million. Upon completion of the offering, we expect our total outstanding long-term indebtedness to be approximately $11.1 million, including approximately $10.3 million under our credit facility and $0.8 million of other indebtedness. Our payments of principal and interest on the indebtedness will reduce the cash available for distribution on the units. We will be prohibited by our credit facility from making cash distributions during an event of default under any of our indebtedness. Furthermore, our leverage and various limitations in the credit facility may reduce our ability to incur additional indebtedness, to engage in some transactions and to capitalize on acquisition or other business opportunities. Any subsequent refinancing of our current indebtedness or any new indebtedness could have similar or greater restrictions.

Federal, state or local regulatory measures could adversely affect our business.

While the Federal Energy Regulatory Commission, or FERC, does not regulate any of our operations, directly or indirectly, it influences certain aspects of our business and the market for our products. As a raw natural gas gatherer we generally are exempt from FERC regulation under the Natural Gas Act of 1938, or NGA, but FERC regulation still significantly affects our business. In recent years, FERC has pursued pro-competitive policies in its regulation of interstate natural gas pipelines. However, we cannot assure you that FERC will continue this approach as it considers matters such as pipeline rates and rules and policies that may affect rights of access to natural gas transportation capacity.

Some of our intrastate natural gas transmission pipelines are subject to regulation as a common carrier and as a gas utility by the Texas Railroad Commission, or TRRC. The TRRC's jurisdiction extends to both rates and pipeline safety. The rates we charge for transportation services are deemed just and reasonable under Texas law unless challenged in a complaint. Should a complaint be filed or should regulation become more active, our business may be adversely affected.

Other state and local regulations also affect our business. We are subject to ratable take and common purchaser statutes in the states where we operate. Ratable take statues generally require gatherers to take, without undue discrimination, natural gas production that may be tendered to the gatherer for handling. Similarly, common purchaser statutes generally require gatherers to purchase without undue discrimination as to source of supply or producer. These statutes have the effect of restricting our right as an owner of gathering facilities to decide with whom we contract to purchase or transport natural gas. Federal law leaves any economic regulation of natural gas gathering to the states, and some of the states in which we operate have adopted complaint-based or other limited economic regulation of natural gas gathering activities. States in which we operate that have adopted some form of complaint-based regulation, like Oklahoma and Texas, generally allow natural gas producers and shippers to file complaints with state regulators in an effort to resolve grievances relating to natural gas gathering access and rate discrimination.

The states in which we conduct operations administer federal pipeline safety standards under the Pipeline Safety Act of 1968. The "rural gathering exemption" under the Natural Gas Pipeline Safety Act of 1968 presently exempts substantial portions of our gathering facilities from jurisdiction under that statute, including those portions located outside of cities, towns, or any area designated as residential or commercial, such as a subdivision or shopping center. The "rural gathering exemption," however, may be restricted in the future, and it does not apply to our natural gas transmission

21

pipelines. In response to recent pipeline accidents in other parts of the country, Congress and the Department of Transportation have passed or are considering heightened pipeline safety requirements. See "Business—Regulation."

Our business involves hazardous substances and may be adversely affected by environmental regulation.

Many of the operations and activities of our gathering systems, plants and other facilities are subject to significant federal, state and local environmental laws and regulations. These include, for example, laws and regulations that impose obligations related to air emissions and discharge of wastes from our facilities and the cleanup of hazardous substances that may have been released at properties currently or previously owned or operated by us or locations to which we have sent wastes for disposal. Various governmental authorities have the power to enforce compliance with these regulations and the permits issued under them, and violators are subject to administrative, civil and criminal penalties, including civil fines, injunctions or both. Liability may be incurred without regard to fault for the remediation of contaminated areas. Private parties, including the owners of properties through which our gathering systems pass, may also have the right to pursue legal actions to enforce compliance as well as to seek damages for non-compliance with environmental laws and regulations or for personal injury or property damage.

There is inherent risk of the incurrence of environmental costs and liabilities in our business due to our handling of natural gas and other petroleum products, air emissions related to our operations, historical industry operations, waste disposal practices and the prior use of natural gas flow meters containing mercury. In addition, the possibility exists that stricter laws, regulations or enforcement policies could significantly increase our compliance costs and the cost of any remediation that may become necessary. We may incur material environmental costs and liabilities. Furthermore, our insurance may not provide sufficient coverage in the event an environmental claim is made against us.

Our business may be adversely affected by increased costs due to stricter pollution control requirements or liabilities resulting from non-compliance with required operating or other regulatory permits. New environmental regulations might adversely affect our products and activities, including processing, storage and transportation, as well as waste management and air emissions. Federal and state agencies could also impose additional safety requirements, any of which could affect our profitability. See "Business—Environmental Matters."

Our use of derivative financial instruments has in the past and could in the future result in financial losses or reduce our income.

We use over-the-counter price and basis swaps with other natural gas merchants and financial institutions, and we use futures and option contracts traded on the New York Mercantile Exchange. Use of these instruments is intended to reduce our exposure to short-term volatility in commodity prices. We currently have in place hedges on 100,000 MMBtu of gas per month at average prices ranging between $2.91 per MMBtu and $3.65 per MMBtu for the twelve month period from October 1, 2002 to September 30, 2003. This quantity represents approximately 80% of the margin on natural gas that we buy at a percentage of index and upon which we are exposed to the risk of fluctuations in natural gas prices. We could incur financial losses or fail to recognize the full value of a market opportunity as a result of volatility in the market values of the underlying commodities or if one of our counterparties fails to perform under a contract. For additional information about our risk management activities, including our use of derivative financial instruments, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosures About Market Risk."

22

Due to our lack of asset diversification, adverse developments in our gathering, transmission, treating, processing and producer services businesses would reduce our ability to make distributions to our unitholders.

We rely exclusively on the revenues generated from our gathering, transmission, treating, processing and producer services businesses, and as a result our financial condition depends upon prices of, and continued demand for, natural gas and NGLs. Due to our lack of asset diversification, an adverse development in one of these businesses would have a significantly greater impact on our financial condition and results of operations than if we maintained more diverse assets.

Our success depends on key members of our management, the loss of whom could disrupt our business operations.

We depend on the continued employment and performance of the officers of the general partner of our general partner and key operational personnel. The general partner of our general partner has entered into employment agreements with each of its executive officers. If any of these officers or other key personnel resign or become unable to continue in their present roles and are not adequately replaced, our business operations could be materially adversely affected. We do not maintain any "key man" life insurance for any officers. See "Management."

Risks Inherent in an Investment in Us

Crosstex Energy Holdings Inc. will own a 70% limited partner interest in us and will control our general partner. Our general partner has conflicts of interest and limited fiduciary

responsibilities, which may permit our general partner to favor its own interests to the detriment of our unitholders.

Following this offering, Crosstex Energy Holdings Inc. will indirectly own an aggregate limited partner interest of approximately 70% in us and will own and control our general partner. Due to its control of our general partner and the size of its limited partnership interest in us, Crosstex Energy Holdings Inc. will be able to effectively control all limited partnership decisions, including any decisions related to the removal of our general partner. Conflicts of interest may arise in the future between Crosstex Energy Holdings Inc. and its affiliates, including our general partner, on the one hand, and our partnership or any of the unitholders, on the other hand. As a result of these conflicts our general partner may favor its own interests and those of its affiliates over the interests of the unitholders. These conflicts include, among others, the following situations:

Conflicts Relating to Control:

23

Conflicts Relating to Costs:

Please read "Conflicts of Interest and Fiduciary Responsibilities" and "Certain Relationships and Related Transactions—Omnibus Agreement."

Our unitholders will have no right to elect our general partner or the directors of its general partner and will have limited ability to remove our general partner.

Unlike the holders of common stock in a corporation, unitholders will have only limited voting rights on matters affecting our business, and therefore limited ability to influence management's decisions regarding our business. Unitholders did not elect our general partner or the board of directors of its general partner and will have no right to elect our general partner or the board of directors of its general partner on an annual or other continuing basis.

Furthermore, if unitholders are dissatisfied with the performance of our general partner, they will have little ability to remove our general partner. The general partner generally may not be removed except upon the vote of the holders of 662/3% of the outstanding units voting together as a single class. Because affiliates of the general partner will control approximately 71.4% of all the units, the general partner currently cannot be removed without the consent of the general partner and its affiliates. Also, if the general partner is removed without cause during the subordination period and units held by the general partner and its affiliates are not voted in favor of that removal, all remaining subordinated units will automatically be converted into common units and any existing arrearages on the common units will be extinguished. A removal without cause would adversely affect the common units by prematurely eliminating their distribution and liquidation preference over the subordinated units which would otherwise have continued until we had met certain distribution and performance tests.

Cause is narrowly defined to mean that a court of competent jurisdiction has entered a final, non-appealable judgment finding the general partner liable for actual fraud, gross negligence, or willful or wanton misconduct in its capacity as our general partner. Cause does not include, in most cases, charges of poor management of the business, so the removal of the general partner because of the unitholders' dissatisfaction with the general partner's performance in managing our partnership will most likely result in the termination of the subordination period.

24

In addition, unitholders' voting rights are further restricted by the partnership agreement provision providing that any units held by a person that owns 20% or more of any class of units then outstanding, other than our general partner, its affiliates, their transferees and persons who acquired such units with the prior approval of the board of directors of the general partner's general partner, cannot be voted on any matter. In addition, the partnership agreement contains provisions limiting the ability of unitholders to call meetings or to acquire information about our operations, as well as other provisions limiting the unitholders' ability to influence the manner or direction of management.

As a result of these provisions, it will be more difficult for a third party to acquire our partnership without first negotiating such a purchase with our general partner and, as a result, you are less likely to receive a takeover premium.

Cost reimbursements due our general partner may be substantial and will reduce the cash available for distribution to you.

Prior to making any distributions on the units, we will reimburse our general partner and its affiliates, including officers and directors of our general partner, for all expenses they incur on our behalf. The reimbursement of expenses could adversely affect our ability to make distributions to you. Our general partner has sole discretion to determine the amount of these expenses. In addition, our general partner and its affiliates may provide us with services for which we will be charged reasonable fees as determined by our general partner in its sole discretion. See "Management—Reimbursement of Expenses of the General Partner."

The control of our general partner may be transferred to a third party, and that third party could replace our current management team, in each case without unitholder consent.

The general partner may transfer its general partner interest to a third party in a merger or in a sale of all or substantially all of its assets without the consent of the unitholders. Furthermore, there is no restriction in the partnership agreement on the ability of the owner of the general partner from transferring its ownership interest in the general partner to a third party. The new owner of the general partner would then be in a position to replace the board of directors and officers of the general partner with its own choices and to control the decisions taken by the board of directors and officers.

Our general partner's absolute discretion in determining the level of cash reserves may adversely affect our ability to make cash distributions to our unitholders.

Our partnership agreement requires our general partner to deduct from operating surplus cash reserves that in its reasonable discretion are necessary to fund our future operating expenditures. In addition, the partnership agreement permits our general partner to reduce available cash by establishing cash reserves for the proper conduct of our business, to comply with applicable law or agreements to which we are a party or to provide funds for future distributions to partners. These cash reserves will affect the amount of cash available for distribution to our unitholders.

Our partnership agreement contains provisions which reduce the remedies available to unitholders for actions that might otherwise constitute a breach of fiduciary duty by our general partner.

Our partnership agreement limits the liability and reduces the fiduciary duties of our general partner to the unitholders. The partnership agreement also restricts the remedies available to unitholders for actions that would otherwise constitute breaches of our general partner's fiduciary duties. If you choose to purchase a common unit, you will be treated as having consented to the various actions contemplated in the partnership agreement and conflicts of interest that might otherwise be considered a breach of fiduciary duties under applicable state law. See "Conflicts of Interest and Fiduciary Responsibilities."

25

You will experience immediate and substantial dilution in net tangible book value of $9.71 per common unit.

The assumed initial public offering price of $20.00 per unit exceeds pro forma net tangible book value of $10.29 per unit. Based on the assumed initial public offering price, you will incur immediate and substantial dilution of $9.71 per common unit. This dilution results primarily because the assets contributed by our general partner and its affiliates are recorded at their historical cost, and not their fair value, in accordance with generally accepted accounting principles. Please read "Dilution."

We may issue additional common units without your approval, which would dilute your ownership interests.

During the subordination period, our general partner, without the approval of our unitholders, may cause us to issue up to 1,166,500 additional common units (1,316,500 additional common units if the underwriters' over-allotment option is exercised in full). Our general partner may also cause us to issue an unlimited number of additional common units or other equity securities of equal rank with the common units, without unitholder approval, in a number of circumstances such as:

The issuance of additional common units or other equity securities of equal or senior rank will have the following effects:

After the end of the subordination period, we may issue an unlimited number of limited partner interests of any type without the approval of our unitholders. Our partnership agreement does not give our unitholders the right to approve our issuance of equity securities ranking junior to the common units at any time.

Our general partner has a limited call right that may require you to sell your common units at an undesirable time or price.

If at any time our general partner and its affiliates own more than 80% of the common units, our general partner will have the right, but not the obligation, which it may assign to any of its affiliates or to us, to acquire all, but not less than all, of the common units held by unaffiliated persons at a price not less than their then-current market price. As a result, you may be required to sell your common

26

units at an undesirable time or price and may therefore not receive any return on your investment. You may also incur a tax liability upon a sale of your units. At the completion of this offering, our general partner and its affiliates will own 14.3% of the common units. At the end of the subordination period, assuming no additional issuances of common units, our general partner and its affiliates will own approximately 71.4% of the common units. For additional information about the call right, please read "The Partnership Agreement—Limited Call Right."

You may not have limited liability if a court finds that unitholder action constitutes control of our business.

You could be held liable for our obligations to the same extent as a general partner if a court determined that the right or the exercise of the right by our unitholders to remove or replace our general partner, to approve amendments to our partnership agreement, or to take other action under our partnership agreement constituted participation in the "control" of our business, to the extent that a person who has transacted business with the partnership reasonably believes, based on your conduct, that you are a general partner. Our general partner generally has unlimited liability for the obligations of the partnership, such as its debts and environmental liabilities, except for those contractual obligations of the partnership that are expressly made without recourse to our general partner. In addition, Section 17-607 of the Delaware Revised Uniform Limited Partnership Act provides that a limited partner who receives a distribution and knew at the time of the distribution that the distribution was in violation of that section may be liable to the limited partnership for the amount of the distribution for a period of three years from the date of the distribution. The limitations on the liability of holders of limited partner interests for the obligations of a limited partnership have not been clearly established in some of the other states in which we do business. Please read "The Partnership Agreement—Limited Liability" for a discussion of the implications of the limitations on liability to a unitholder.

Unitholders may have limited liquidity for their units, a trading market may not develop for the units and you may not be able to resell your units at the initial public offering price.

Prior to the offering, there has been no public market for the common units. After the offering, there will be only 2,000,000 publicly-traded units. We do not know the extent to which investor interest will lead to the development of a trading market or how liquid that market might be. You may not be able to resell your common units at or above the initial public offering price. Additionally, the lack of liquidity may result in wide bid-ask spreads, contribute to significant fluctuations in the market price of the common units and limit the number of investors who are able to buy the common units.

Restrictions in our credit facility could limit our ability to make distributions to our unitholders.